Paul Morigi

A True Dividend Stock Without A Dividend

Having been a Warren Buffett fanatic since the beginning of my investing journey, Berkshire Hathaway (BRK.A) (NYSE:BRK.B) was one of my largest holdings for a good while. I eventually became more of a Mohnish Pabrai-style cloner, and after reading enough 13F filings, realized Berkshire resembled the DJIA 30 to some extent at that time.

Thereafter, I jettisoned my Berkshire and started to self-index. Now that my dividend income is rather significant in taxable accounts, Berkshire is becoming an attractive option once again to collect dividends and avoid taxes. In a way, buying a holdings company like Berkshire Hathaway is like being able to operate a tax advantaged account within a taxable brokerage.

While Berkshire is now more of an amalgamation of decision-makers rather than a vertical business, the top 10 holdings are almost all dividend payers chosen by the top dog. On top of that, Berkshire owns some great private businesses that allow for more cash to be deployed into the holdings segment of the business.

History

The Berkshire Hathaway story is so well known that I don’t want to add too much context to the ether of information. In essence, Warren Buffett took over a textile company which he then slowly leveraged into a conglomerate of private businesses combined with a holdings company of publicly listed stocks. The ethos is to avoid paying a dividend to mitigate double taxation and compound earnings and dividends at a more tax-advantaged rate than a normal corporation would. The tethering back and forth of choices between deployment of capital into private acquisitions versus publicly listed holdings presents several unique opportunities to the business.

From the 10K:

Berkshire Hathaway Inc. (“Berkshire,” “Company” or “Registrant”) is a holding company owning subsidiaries engaged in numerous diverse business activities. The most important of these are insurance businesses conducted on both a primary basis and a reinsurance basis, a freight rail transportation business and a group of utility and energy generation and distribution businesses. Berkshire also owns and operates numerous other businesses engaged in a variety of manufacturing, services, retailing and other activities. Berkshire is domiciled in the state of Delaware, and its corporate headquarters is in Omaha, Nebraska.

Amongst the larger private investments, we can see utility/energy, insurance, and rail as the primary investments of choice on the private side. These businesses have a durable competitive advantage in that they are necessary to make the economy function.

- All companies and individuals require insurance. The premiums or “float” of insurance can be invested into short risk free liquid securities and stocks. Astute risk management makes this an amazing business in the right hands.

- Freight transport is necessary to move bulk goods cheaply and efficiently across North America. There are few substitutes to move bulk goods by land in a similar quantity to energy expenditure.

- Energy/utilities are inelastic. They are regulated, but the consumer will pay the price up to the allowed regulation.

Chart

The stock is not far off its high. Berkshire has performed very well relative to the market the past year due to the Apple (AAPL) holding combined with the amazing net worth of the company. The market has been risk off and Berkshire’s lack of risk due to the net worth was attractive. The Regional Bank liquidity crisis was one major thorn in the market’s side. Berkshire was viewed as a scion of good capital management. It is and was one of the most conservative plays in the market due to the balance sheet.

Over time Berkshire has done very well. The upward trajectory moves with the S&P 500 with a couple of points of alpha depending on your entry point. Now approaching this massive size in market cap, I have started to treat Berkshire as a tax-advantaged index fund with a 1.4% dividend demonstrated in the average yield of the top 10 holdings.

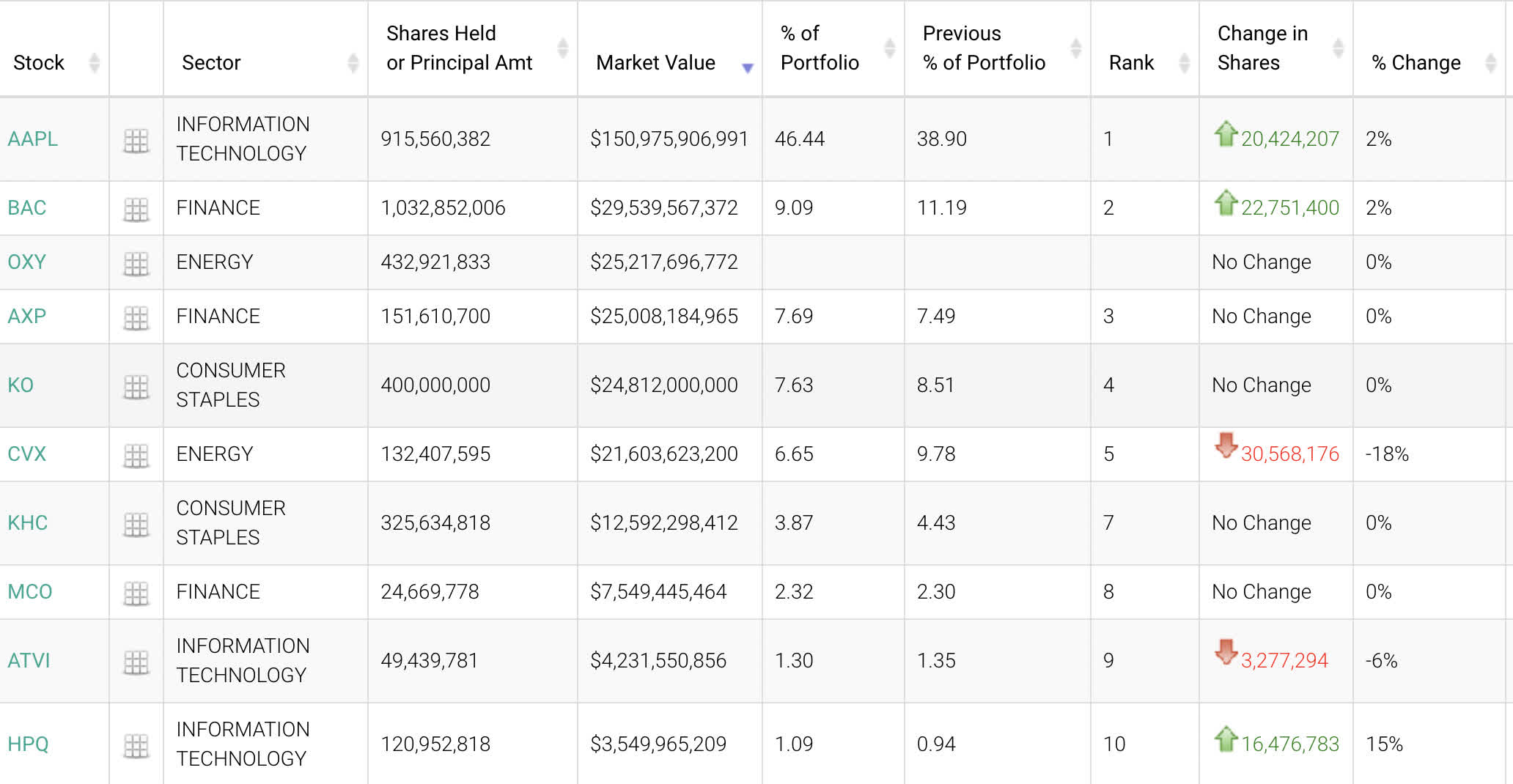

Top 10 holdings

Whale Wisdom Berkshire MRQ 13F

{kind=link}

Top 10 Dividend yields, coverage, and growth

Since only 9 of the top 10 have a dividend, we’ll break down those 9 by yield, payout ratio, and dividend growth. The odd man out is Activision (ATVI), which was an arbitrage play. This top 10 makes up 93.7% of the Berkshire Hathaway portfolio. So, it’s pretty accurate to say that the lump sum of our dividends will be derived from this segment.

| STOCK | YIELD | PAYOUT | 5 YR GROWTH |

| Apple (AAPL) | .53% | 15.62% | 7.26% |

| Bank of America (BAC) | 3.01% | 26.13% | 12.89% |

| Occidental Petroleum (OXY) | 1.21% | 6.87% | NG |

| American Express (AXP) | 1.4% | 22.7% | 9.53% |

| Coca-Cola (KO) | 3.04% | 70.63% | 3.48% |

| Chevron (CVX) | 3.8% | 30.4% | 5.9% |

| Kraft Heinz (KHC) | 4.34% | 55.94% | NG |

| Moody’s (MCO) | .92% | 33.14% | 12.38% |

| HP Inc. (HPQ) | 3.52% | 29.8% | 13.51% |

Within the portfolio of Berkshire holdings, this segment yields about 1.43% and a tad over a 6% growth rate within the collection of holdings. We should consider this our baseline dividend yield for Berkshire Hathaway holdings currently.

Japanese plays

Another well-known factor is that Berkshire has leveraged itself into the Japanese stock market. Not reflected in the 13F filings and held under a private subsidiary, the company now has $15+ Billion tied up in Japan:

I recently did an article on another great Japanese play, Panasonic Holdings Corporation, where I went over the intrinsic values of Buffett’s Japanese plays according to the Graham Number, all were and are trading at a discount:

| Ratios | Book Value | TTM EPS | Graham Number |

| Itochu | 47.36 | 8.22 | |

| Mitsubishi | 40.02 | 6.17 | |

| Sumitomo | 13.32 | 3.55 | |

| Mitsui | 580.96 | 103.81 | |

| Marubeni | 117.63 | 23.80 |

Almost all of these stocks pay good dividends, are quality companies, and trade below Ben Graham’s fair deal value where the P/E X the P/B does not cross 22.5. This used to be the norm in the US, but good deals along those ratios are almost exclusively limited to financials and some utilities at this point. Every other unregulated industry trades at a significant premium of assets.

The billionaire CEO explained during his company’s recent shareholder meeting that he broke from tradition because the Japanese wager was such a no-brainer. The businesses were large enough to move the needle at Berkshire, traded cheaply, operated in a broad range of familiar industries, and several of them paid dividends and repurchased their shares, he said.

“They’re doing intelligent things, and they’re sizable, so we just started buying them,” Buffett recalled. “We are $4 billion or $5 billion ahead plus dividends.”

Buffett emphasized that the stocks were absolute bargains during a recent trip to Tokyo. He described their valuations as “ridiculous” relative to prevailing interest rates.

Even more non-double taxed dividends to add to the tax-advantaged pile. I concur that Japan is a nice opportunity, conservative, and cheap since the Nikkei is a relatively slow market since the 1980s. Being able to issue bonds in Japan, borrow at lower rates than here, and buy intrinsically undervalued stocks directly with the proceeds if desired seems like a dream come true.

Subsidiaries

Take a look at the numerous Berkshire Hathaway subsidiaries list. The profits from the privately held side of the business are dividends in themselves as well that can be reinvested into stocks or into growing the businesses. They can also just let the cash proceeds pile up and collect a conservative 5% in short term debt on the cash and cash equivalents line.

Balance Sheet

The most important observation of the Berkshire Hathaway Balance sheet according to Warren Buffett is the spread between Total Assets and Total Liabilities or Net Worth. Cash and cash equivalents are also an important factor:

MRQ Balance Sheet Number:

- Total assets $997,072- Total Liabilities $480,812= $516,260 Billion in Net Worth.

{kind=link}

With a large cash pile, Berkshire can also return a risk free 5+% from short term debt and still remain highly liquid. Ready to pounce on a deal.

Valuation

Warren Buffett always said he thought Berkshire was worth at least 1.25 X book value as a baseline. He would buy back shares there. This incorporated “the float” of the well-run Berkshire insurance businesses that could invest your insurance premiums in short-term debt and collect a check for your monthly payment. As long as the payouts didn’t exceed the incoming premiums, you were sure to make a profit. Sounds simple enough but many fail. With Ajit Jain at the helm, Berkshire has been an underwriting stalwart. With the short and long-risk-free rates now being so significant compared to the decade prior, this could yield a lot of cash for Berkshire Hathaway.

Let’s take a look at the Berkshire Hathaway valuation based on the Graham Number, which is a popular way to analyze asset-heavy companies, and financial and insurance institutions, for which Berkshire Hathaway qualifies as that. It is a price where the P/E ratio X the price-to-book ratio does not exceed 22.5.It was first described in the original Intelligent Investor.

The data will be based on the A shares as screeners go haywire when converting the A and B share values.

Data courtesy of Seeking Alpha

- 2023 estimated EPS $23.14K a share

- TTM Book value $347,828

- Square root 22.5X 23,140 X $347,828 =$425,554 A share value

- Current price $508,811

- 16% premium to intrinsic value

As the discount/premium ratio carries the same weight across both classes because they both have voting rights, we can also apply this 16% deduction to the B shares to find a fair value. Based on numbers as of June 12th, 2023, that would be:

- $333 X 83.7%= $278.72/B share value

Ed Thorp

From Wikipedia:

Thorp is the author of Beat the Dealer, which mathematically proved that the house advantage in blackjack could be overcome by card counting. He also developed and applied effective hedge fund techniques in the financial markets, and collaborated with Claude Shannon in creating the first wearable computer.

Thorp received his Ph.D. in mathematics from the University of California, Los Angeles in 1958, and worked at the Massachusetts Institute of Technology MIT from 1959 to 1961. He was a professor of mathematics from 1961 to 1965 at New Mexico State University, and then joined the University of California, Irvine where he was a professor of mathematics from 1965 to 1977 and a professor of mathematics and finance from 1977 to 1982.

He was well known for his options hedge fund, Princeton/Newport Partners, which he ran around the same time his contemporary Jim Simons left academics to start his ultra-famous Renaissance quant fund. He claims his investments yielded an annualized 20 percent rate of return averaged over 28.5 years. This is largely a result of Berkshire Hathaway.

Ed Thorp also views Berkshire in a similar way to the thesis laid out in this article. From a past Barron’s interview:

Q: What’s in your portfolio now?

A: One good stroke of good fortune was meeting Warren Buffett in 1968. It led me to realize that I needed to invest in Berkshire Hathaway (ticker: BRK.A), although I didn’t do it until 1982. It’s my single investment in the stock market. It’s like a broad value-stocks equity index. I hold it in lieu of VTSAX [the Vanguard Total Stock Market fund]. It does about as well with no current taxes to pay. VTSAX has dividends that are taxed annually. I also have some hedge funds, but I consider them not as good as Berkshire, so I use them to spend and finance other things I do.

Risk

A couple of items could be negatives for Berkshire stock. The first is the excessively large position in Apple. Many, including myself, have noted the rich valuation of this amazing tech titan. While other large brethren in the Nasdaq have gone through a 30-50% haircut and have started to retrace, Apple has not. If we are in a new bull market, Apple will continue its elevation, if not, Apple has the biggest risk of wiping out value on the Berkshire Hathaway holdings side.

On the private business side, there are headwinds in insurance, rail, and energy businesses as alluded to in the most recent Berkshire Hathaway shareholder meeting. One fresh off the presses issue regarding the energy division has Berkshire Hathaway being found liable in an Oregon wildfire that it was determined by a jury to have erupted from a Berkshire Hathaway subsidiary PacifiCorp utility line.

The desire to take businesses whole, and avoid the dividend taxation from profit distribution on the corporate side cuts both ways. Yes, you get the profit directly sent to the parent, but the parent can also be exposed to liability from the subsidiary. This also goes for the rail division. BNSF’s rail operations transport hazardous chemicals across state lines in an industry that has seen a recent spate of derailments. The rail division has already come under a lawsuit regarding the outsourcing of its’ locomotive repair and maintenance. With the rail businesses being under greater scrutiny than ever, there won’t be any room for cost-cutting in the business.

Finally, cars and their replacement costs are still overpriced, Geico faces headwinds from this as do other vehicle insurance companies.

{kind=link}

Vehicles insured within the covid era where the vehicle was underwritten at one value but would need to be replaced at a greater one is an issue. Although the short end of the yield curve is a tailwind, replacement costs are a headwind.

Conclusion

Similar to Thorp, I’m starting to warm up to the treatment of Berkshire Hathaway as a great index fund substitute for the broad market indexes funds like SPY (SPY) or VTSAX. Even if not trading exactly at intrinsic value, neither do the index funds if you consider intrinsic value at 15 X current or forward EPS for the broader market. The company will not always be run by Buffett and Munger, but the well-documented strategies should be easily carried forward by the management team.

As pointed out in the risks section, Berkshire Hathaway is not just a large, glorified holdings company. They have a significant segment of privately owned businesses that can both ratchet up profitability or hurt it through liability and underperformance. I still believe in most years the private segment will add more positives than negatives to the overall Berkshire operating results. Warren Buffett however has indicated that 2023 will probably not be a great year for the privately held bunch.

For those overloaded with dividends, the Berkshire Hathaway dividend machines may be a great way to add some income to the portfolio that you simply sell long-term shares at whatever percent you need to supply yourself with income. The dividends are there, the compounding is internal. Berkshire is especially great for liquid brokerages.