bymuratdeniz/iStock via Getty Images

The next meeting of the Federal Open Market Committee, the Federal Reserve group that sets monetary policy, is scheduled to meet on June 13 and 14.

The meeting after that will be on July 25 and 26.

There will not be a meeting in August.

Right now, it seems as if traders are looking for no increase in the Fed’s policy rate of interest in June, followed by another increase in July.

“Pricing in the Treasury futures market now firmly points to a quarter-point interest rate rise by the US Federal Reserve in July after a pause in June, while expectations of rate cuts for later this year have fallen….”

“Strong US economic data in recent weeks, including a robust jobs report, have fueled these bets, which traders added to after the decisions in Canada and Australia.”

The U.S. economy just keeps putting out signs of strength amidst other signs that some weaknesses are starting to show up.

So, the Fed says, it wants to see more data.

And, then the U.S. Treasury faces the need to raise somewhere around $1.0 trillion in the capital markets. Yes, the problem about the debt ceiling has been resolved, but, now the Treasury needs to replace its cash shortage, a shortage that was created due to the debt ceiling battle.

The forecast here is for further market rate increases.

So, the Fed wants to see more data.

Well, that is all fine and good for the bond market, but what about the investors in the stock market?

Headlines leading off the second section of the Wall Street Journal read

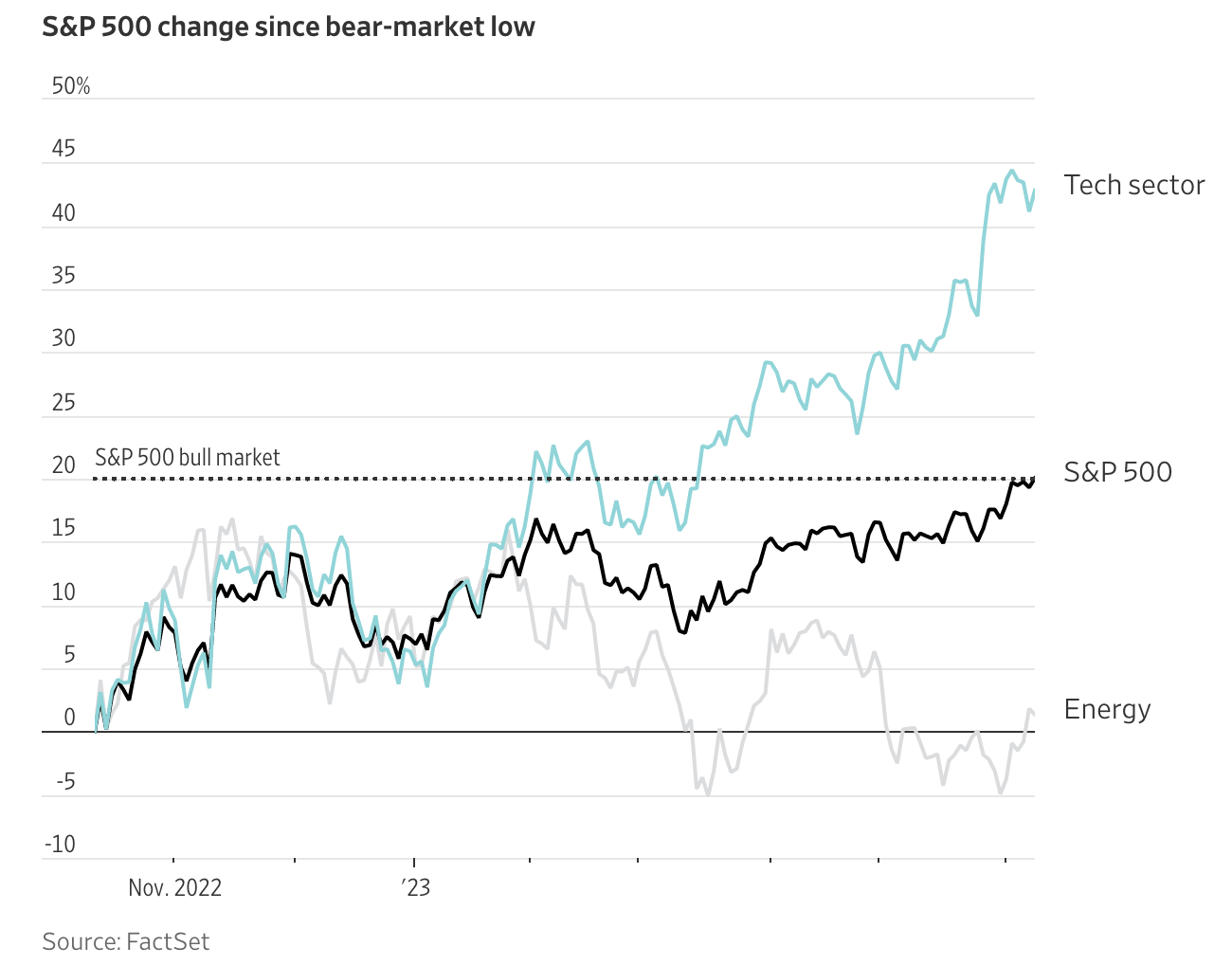

“S&P 500 Starts a New Bull Market.”

The index rose on Thursday, finishing up 20 percent from its October low. That signals the start of a bull market.

But, be careful.

“The broad index powered higher over the past few months, in large part because of a handful of companies posting outsize gains.”

S&P 500 Change since start of Bear Market (Wall Street Journal)

{kind=link}

Investors have been waiting most of this year for the Federal Reserve to “pivot” from its tight monetary stance.

Now, investors in the stock market seem to be waiting for the Federal Reserve to “pause” in its efforts to increase its policy rate of interest.

But, whether or not the Fed “stays still” at the June meeting remains to be seen.

The most interesting thing, to me, in the above chart, is the split in the market.

This, to me, is another indication of how “mixed up” the U.S. economy is.

Investors see the technology sector as “booming,” but they also see a lot of other areas in the economy as particularly weak.

And, this is something that Federal Reserve officials must incorporate into their decision-making.

A lot has happened over the past three or four years and this has resulted in many, many cases of disequilibrium.

The jobs market in the U.S. seems particularly strong. Yet, we hear of layoffs here and layoffs there. Labor conditions depend upon what sector of the economy you are looking at.

Inflation has been moving downward since June 2022, core inflation, which removes volatile food and energy prices, has barely changed since the end of last year.

Some sectors of the economy are moving ahead well. Others are not.

And, then there are supply chain disturbances.

And, then there are national collisions, wars, going on in the world.

And, there still seems to be an excessive amount of money floating around the economy, trying to find good places to rest.

Nothing seems to be still.

Yet, many investors believe that the Federal Reserve is going to back off.

And, the U.S. Treasury Department is going to get its act in order. But, do Ms. Yellen and the U.S. Treasury Department really know what the future fiscal policy is going to look like?

Investors keep hoping.

Federal Reserve Actions

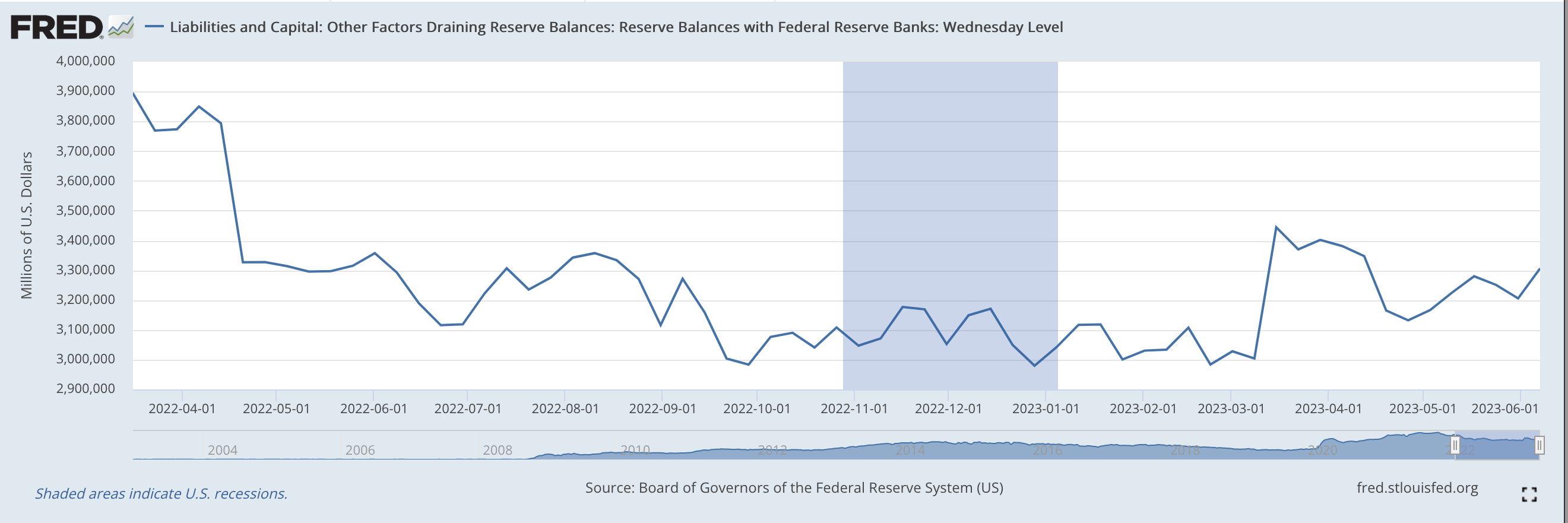

Speaking of the U.S. Treasury Department, the Treasury actually increased its deposits in its General Account at the Fed last week after weeks of decline.

As alluded to above, the Treasury Department has been paying down its General Account over the past month or so as the debt ceiling battle continued.

Now, it is in the process of building this up.

But, as the Treasury gets money through the open market to raise its cash balances, the Fed will need less money coming in through the reverse repurchase agreement vehicle to manage bank liquidity.

Last week, as the Treasury Department increased the funds in its General Account by $16.6 billion, the amount of money coming into the Fed through reverse repos dropped by $107.6 billion.

So, as the increase in the General Account removed money from the banking system, the decline in the reverse repos added money to the banking system.

Overall, Reserve Balances at Federal Reserve Banks increased by $100.7 billion. That is, the liquidity in the banking system rose as the U.S. Treasury Department gets back into a more “normal” operating position.

Reserve Balances With Federal Reserve Banks (Federal Reserve)

{kind=link}

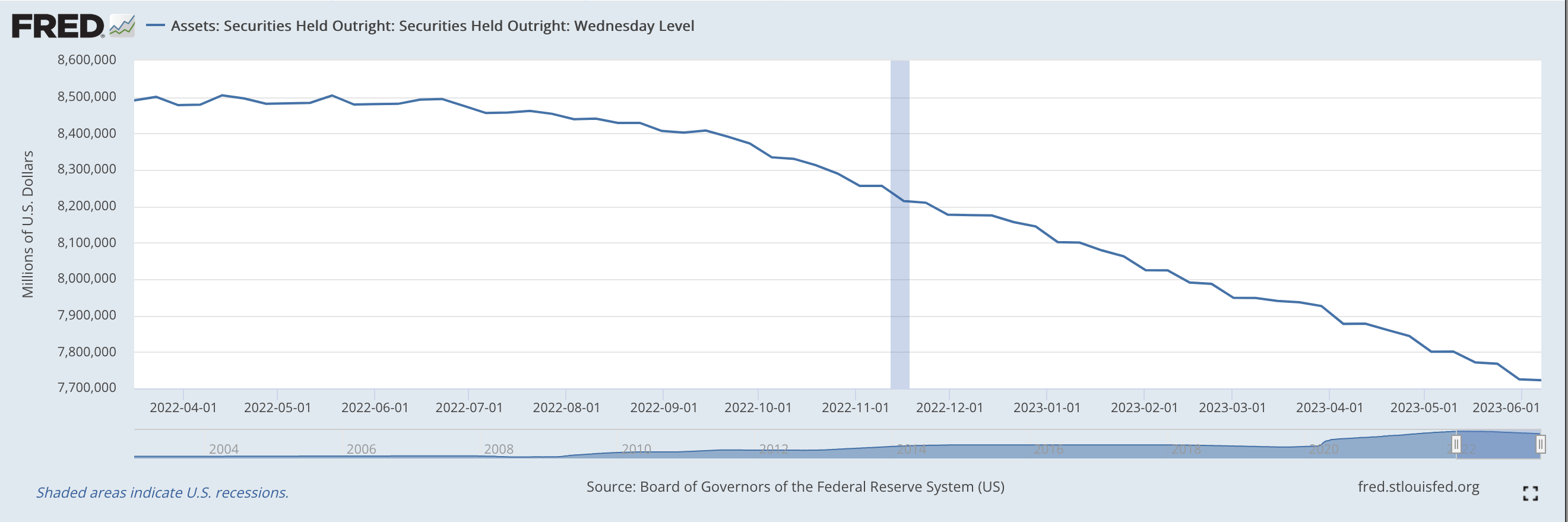

The Federal Reserve continued its program of quantitative tightening as it oversaw a $2.4 billion reduction in its securities portfolio in the latest banking week, bringing the total decline in securities held outright since March 16, 2022, to $768.1 billion.

Taking into account the changes in the “unamortized” premiums and discounts associated with these securities, the overall effect on the Fed’s balance sheet was a $823.2 reduction since March 16, 2022.

Here is the picture of the Fed’s securities held outright.

Securities Held Outright (Federal Reserve)

{kind=link}

So, the Federal Reserve is staying with its program to reduce the amount of securities it holds on its balance sheet.

How much longer this will go on is totally unknown, but this is the ultimate program connected with the Fed’s going into a “pivot” or not.

Future

Next week we will have the results from the next Federal Open Market Committee meeting.

Right now, it looks as if the FOMC will not move its rate.

But, in this environment, things could change overnight. So, hang on, be prepared to be surprised.

To me, the world seems so filled with uncertainty that almost anything could happen.

I still believe that the Federal Reserve has a ways to go in terms of raising its policy rate of interest. The Fed still has to make up for all the liquidity it injected into the banking system during the early stages of the Covid-19 pandemic. That is, the Fed created “asset price bubble” has a lot more downside to it than, I think, has been recognized by the policy makers.

Furthermore, the Fed still has to deal with a Washington D.C. administration that likes to spend and spend and spend.

This is just going to add more pressure to the Fed’s decisions and will also add more disequilibrium to just where the economy is.

One result…more market volatility.

Everyone is going to be looking toward the Fed!