lvcandy/iStock via Getty Images

Enterprise Products Partners (EPD) and Plains All American Pipeline L.P. (NASDAQ:PAA) are two of the more profitable pipeline companies in the USA. Although similar in revenue, EPD has about 6 times the market cap of PAA.

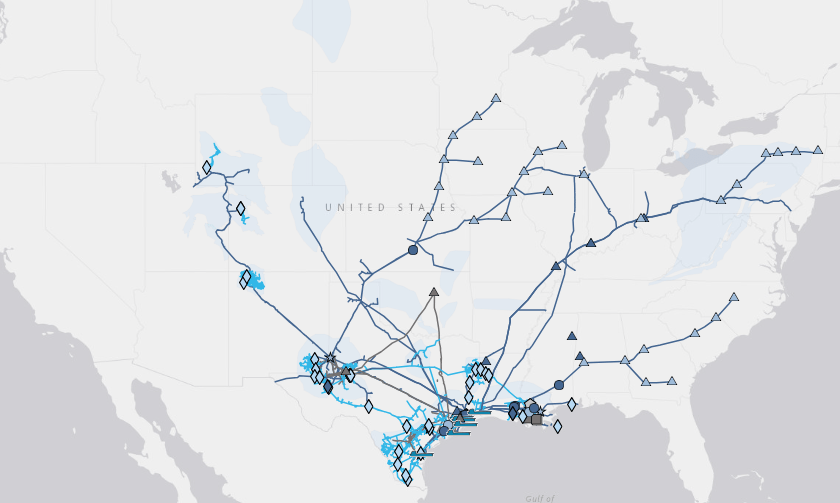

With operations spanning North America, EPD generates huge amounts of revenue and cash flow.

{kind=link}

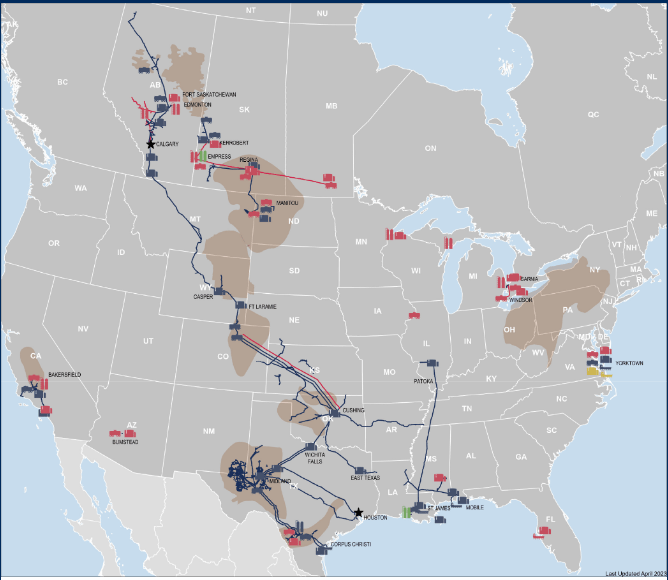

PAA, on the other hand, mainly covers the middle area of North America, extending from Canada to Mexico.

{kind=link}

Although they don’t compete directly with each other, their differences in business practices and management are constant themes here on Seeking Alpha.

But with collapsing banks, higher interest rates, and a potential recession on the horizon, every asset-heavy stock is at risk to some extent.

In this article, I will compare the two’s potential based on what may go right or wrong over the next 12 months.

Note that I use the terms “distribution” and “dividend” interchangeably.

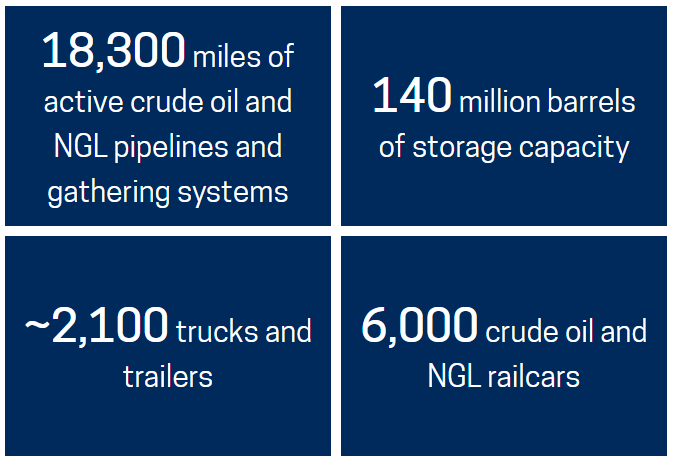

1. With a combination of more than 68,000 miles of pipelines, EPD and PAA pipelines span North America

EPD (50,000+ miles) and PAA (18,000+ miles) have an enormous pipeline footprint. Both companies have their major concentrations of production facilities in Texas and are headquartered there, EPD in Dallas and PAA in Houston.

PAA has more associated assets than EPD including storage facilities, trucks, and railcars.

{kind=link}

2. Financial metrics

When we look at the financial metrics comparing the two companies on a TTM (Trailing Twelve Month) basis which in this case is the 2022 fiscal year for both companies, several metrics jump out indicating how underpriced PAA is versus EPD.

Seeking Alpha and author

We can see that PAA’s price-to-sales ratio (Line 3) is 20% of EPD’s but EPD’s Gross Margin (Line 5) is much higher than PAA’s 12% to 5%. But when we look at GM/Market Value (Line 8) PAA’s margin is more than twice EPD’s 28% to 12%. Those comparisons indicate that either PAA is underpriced or EPD is overpriced relative to each other.

However, PAA’s more conservative approach to debt shows an advantage relative to EPD’s as can be seen by the Debt/EBITDA ratio (Line 14) and that is taking into account EPD’s overall impressive credit profile.

When it comes to Price to Free Cash Flow (Line 16), PAA is selling at a much cheaper price than EPD. This may also imply that PAA is undervalued relative to EPD.

And finally, the Dividend Rate (Line 18) shows both companies are above 7%.

So, based on the above metrics, PAA looks relatively undervalued compared to EPD.

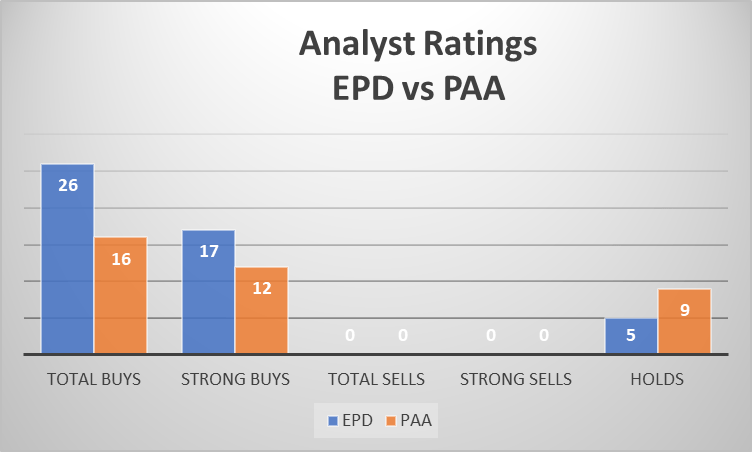

3. Analysts’ ratings show both companies are extremely well-liked by analysts but not so much by quants

Both Seeking Alpha writers and Wall Street analysts love, love, love these two stocks. The total of 42 Buy recommendations with 29 of those being Strong Buys and zero Sells, is one of the best 2 company ratings I have seen in any of my comparison articles.

{kind=link}

Interestingly enough, quants are not nearly as excited as the analysts about EPD, with a very modest “Hold” call for the last 12 months.

{kind=link}

However, quants think PAA has a lot of potential with nothing but Buy ratings since March and some Strong Buys in there too.

{kind=link}

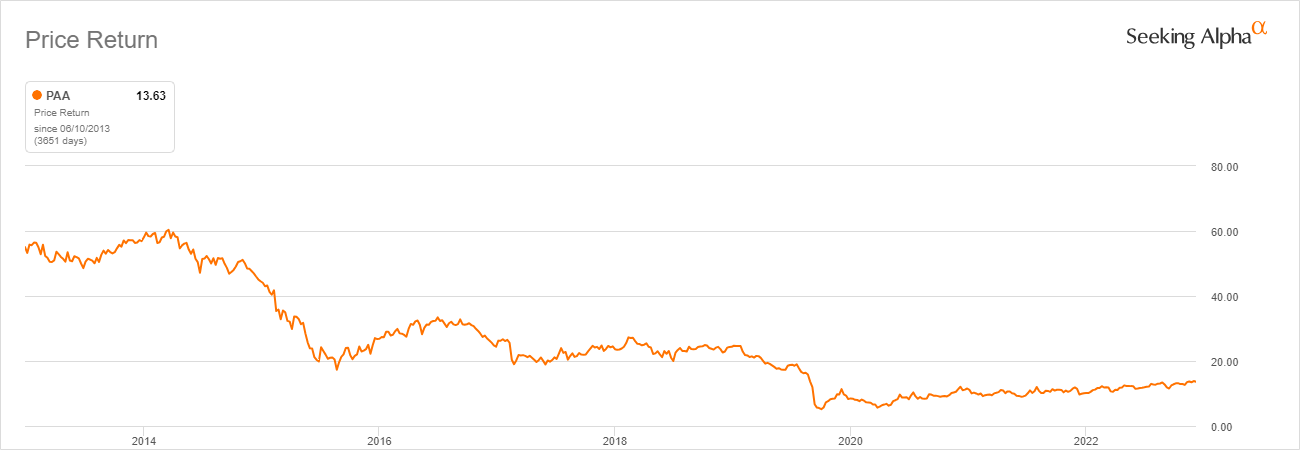

If we look at the prices for midstream companies from 2014 to the present, we can see a decided downward trend. That’s 9 years and counting.

Author

So when considering any pipeline company, look carefully at the historical record shown above. It doesn’t mean they won’t go up from here, but there is a strong hint that the upside will be limited.

Note that the carnage is universal, and even a conservative stalwart like EPD has seen a crushing decrease in the share price since 2014.

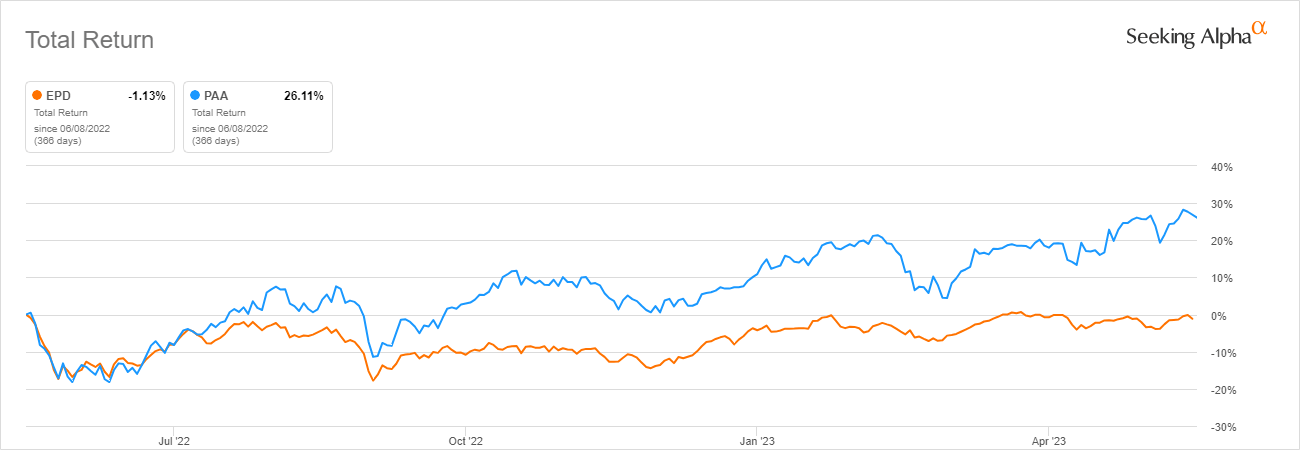

The following chart compares EPD versus PAA on a total return basis (including dividends) over the last 12 months. It shows that over that time period, PAA returned a very healthy profit of 26% to investors while EPD lost 1%.

{kind=link}

4. Dividend history

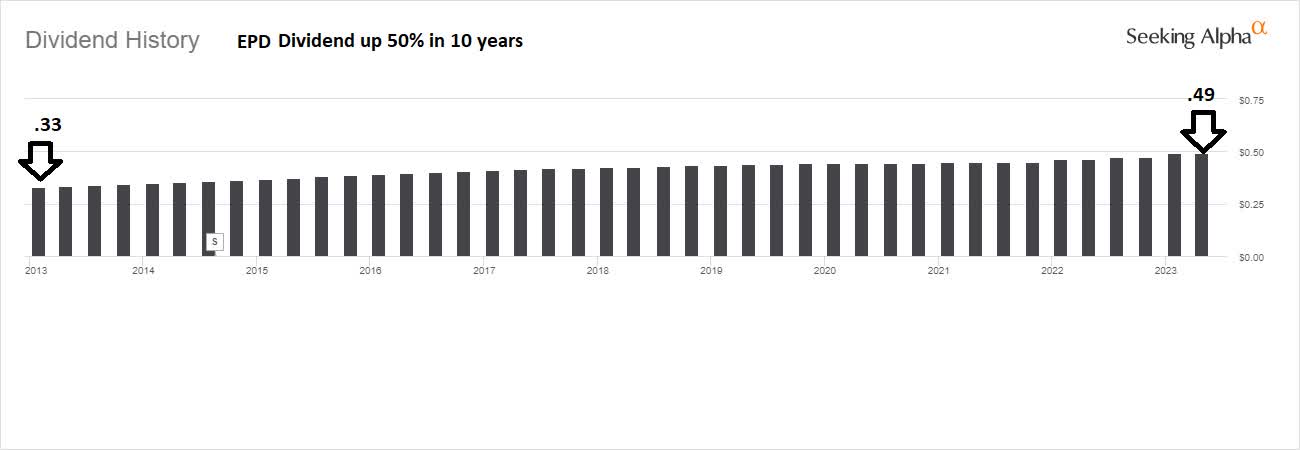

EPD has raised its dividend every year for the past 23 years, a very impressive record indeed. However, it has taken EPD 10 years to raise its dividend rate by 50%.

{kind=link}

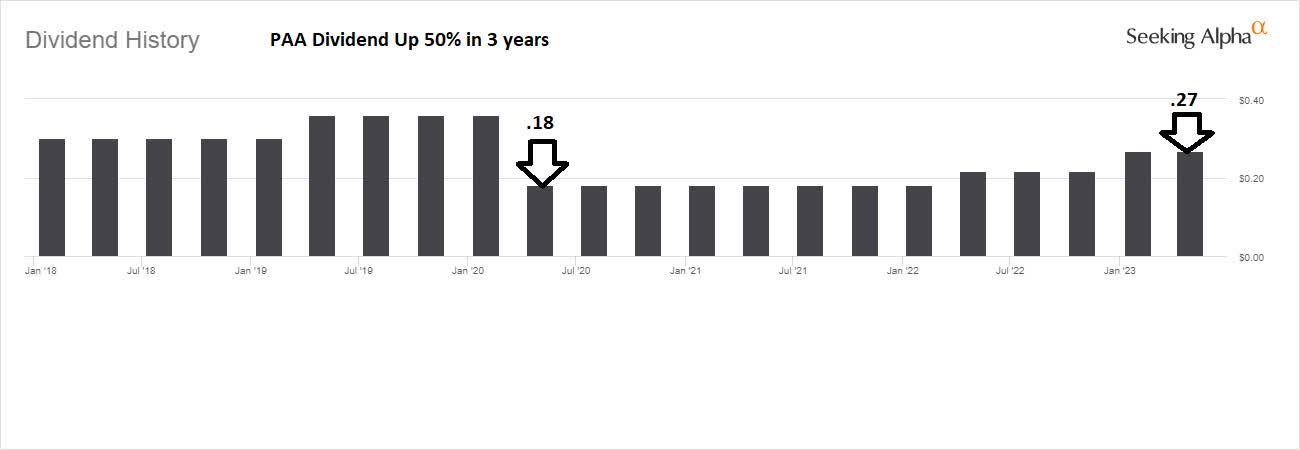

PAA on the other hand, has had a much worse long-term historical record. But since it reduced its dividend in 2020 it has raised it by 50% in only 3 years compared to EPD’s 50% in 10 years.

{kind=link}

Obviously, in terms of long-term safety, EPD’s dividend record is superb. But over the short term, PAA has vastly outperformed EPD and is likely to continue to do so at least over the next few years.

Since both dividend rates are currently in the 7% range, PAA is the obvious winner for the possible rapid rate of future dividend increases.

Conclusion

Pipelines are not the market’s favorite pick right now and likely won’t be in the future either. ESG and negative political headwinds will plague the market for the foreseeable future.

But that doesn’t mean that there is no potential in any MLPs. In PAA’s case, the price is low enough that if it just gets back to the MLP median value on a P/E ratio and FCF (Free Cash Flow) basis, it could have a significant upside to at least $18 and maybe $20. And in the meantime, it’s paying a healthy and growing 7% distribution.

But even if PAA is at $20 it would still be far below its historical high of about $60.

{kind=link}

On the other hand, EPD is conservatively managed and has raised its distribution for 23 straight years albeit slowly. But I don’t see how you get much if any capital appreciation from EPD over the next year or so, at least compared to PAA.

Plains All American stock is a Buy as a turnaround candidate with an extremely high and rapidly growing distribution yield.

EPD stock is a hold.