da-kuk

Introduction

In March I wrote a bullish SA article about U.S. air pollution control technology firm Fuel Tech (NASDAQ:FTEK) in which I said that 2023 revenues could surpass $30 million and that strong financial results over the next few quarters could boost the share price to levels of about $1.50

In my view, the Q2 2023 financial results of Fuel Tech were underwhelming, and considering the share price is approaching $1.40, I’m no longer comfortable with keeping a buy rating on the stock. The company is still in the red and the order backlog is falling, and at this market valuation level, I’m changing my stance to neutral. Let’s review.

Overview of the Q1 2023 financial results

In case you’re not familiar with Fuel Tech or my earlier coverage, here’s a short description of the business. The company was established in 1987 and it focuses on the development and application of multi-pollutant emissions control and water treatment technologies in the USA. It also sells air pollution control systems abroad and the business comprises two units, namely Air Pollution Control, and Fuel Chem. The Air Pollution Control segment includes technologies for the reduction of NOx emissions in flue gas from firing natural gas or coal from boilers, incinerators, and furnaces. These include over-fire air systems, selective non-catalytic reduction systems, and selective catalytic reduction systems. This segment accounts for about half of revenues and its clients include coal and natural gas plants among others. Fuel Chem, in turn, specializes in chemical injection processes for the control of slagging, fouling, corrosion, opacity, and other sulfur trioxide-related issues in coal-fired furnaces and boilers. Fuel Tech also has a patent-pending channel injector and a patent-pending saturator technology for the delivery of supersaturated oxygen solutions and other gas-water combinations to target process applications or environmental issues. It’s an alternative to conventional water and wastewater treatment aeration and the company plans to commence its first on-site demonstration at an aquaculture setting in the USA in late Q2 or early Q3 2023. Fuel Tech is targeting a global sales pipeline of $50 million to $75 million, and its customers include Enel (OTCPK:ENLAY) (OTCPK:ESOCF), Endesa (OTCPK:ELEZF) (OTCPK:ELEZY), and Engie (OTCPK:ENGIY) (OTCPK:ENGQF) among others. The breakeven annual revenue is typically around $25-30 million depending on the product segment mix.

Fuel Tech

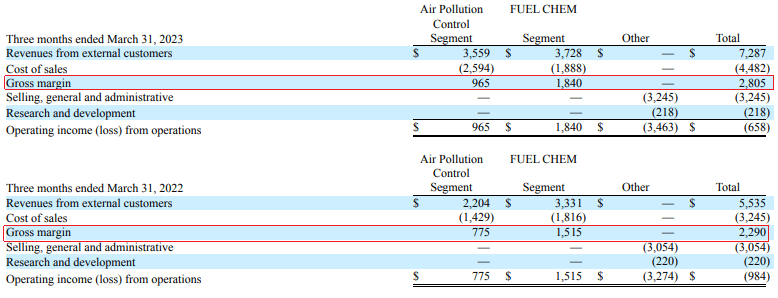

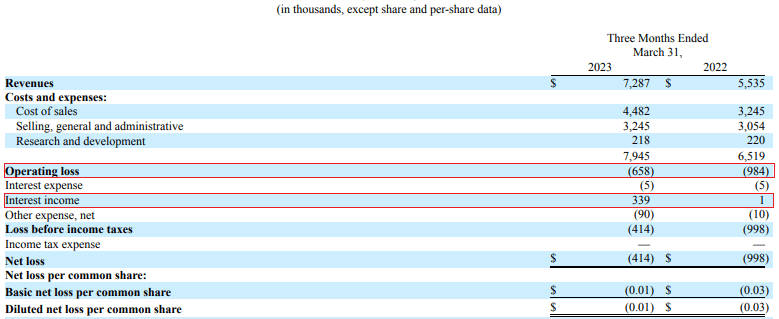

Looking at the Q1 2023 financial results, revenues jumped by 31.7% year on year to $7.29 million thanks to the strong performance of the Air Pollution Control segment. The revenues of the latter soared by 61.5% to $3.56 million thanks to the timing of project execution as well as new orders announced in 2022 which were delivered during the period. The revenue of the Fuel Chem segment, in turn, rose by 11.9% to $3.73 million as increased energy demand in the USA positively impacted coal-fired dispatch in areas where the company has programs installed. Yet, I’m disappointed that the gross profit margin of both segments declined. This brought the combined gross profit margin down to 38.5% from 41.4% a year earlier. Fuel Tech attributed the decrease to product and project mix, and I’m concerned that there don’t appear to be economies of scale here, especially in the Air Pollution Control segment.

{kind=link}

Fuel Tech

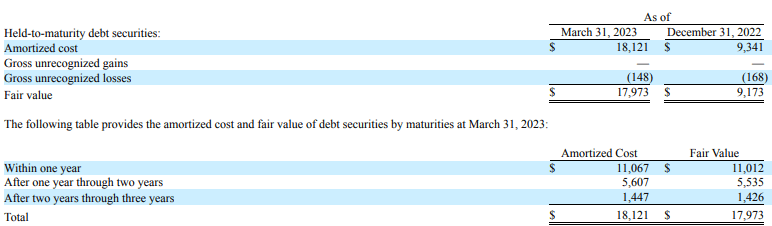

In addition, selling, general and administrative expenses rose by 6.3% year on year to $3.25 million due to increases in employee compensation and benefit-related costs. As a result, Fuel Tech closed Q1 2023 with an operating loss of $0.66 million. On a positive note, interest income soared to $0.34 million as the company boosted its investments in US Treasury securities to $17.97 million from $9.17 million as of December. Fuel Tech said during its Q1 2023 earnings call that it expects interest income for the full year to come in at around $1.2 million.

{kind=link}

Fuel Tech

{kind=link}

Fuel Tech

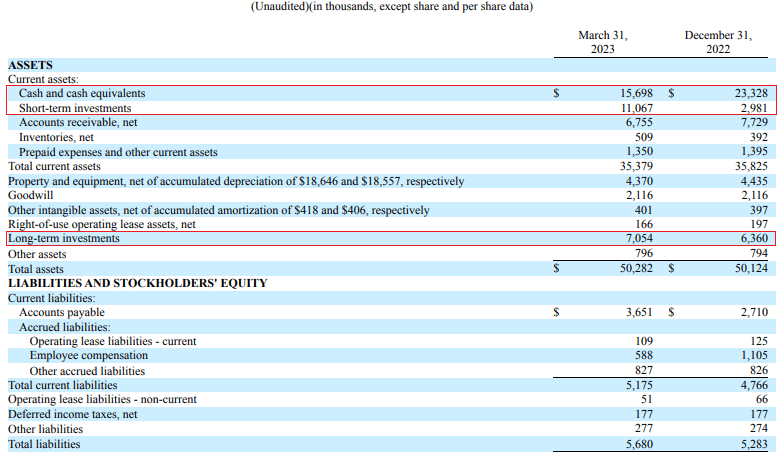

Turning our attention to the balance sheet, Fuel Tech finished Q1 2023 with cash and cash equivalents of $15.7 million and I expect investments in US Treasury securities to increase further during the coming months. In 2022, the board approved a plan to invest up to $20 million of excess capital in debt securities. The company has an asset-light business model and there are no significant capital expenditures planned for the remainder of 2023.

{kind=link}

Fuel Tech

Overall, Fuel Tech has no debts, and cash and US Treasury securities were $33.82 million as of March compared to a market capitalization of $41.91 million as of the time of writing. That being said, I’m concerned that the company could fall short of meeting its forecasts for sales of between $27 million and $32 million for 2023 considering the order backlog is shrinking despite $5.2 million of new orders announced in February. The consolidated backlog of the company went down by $0.66 million quarter on quarter to $7.59 million as of March 2023. In my view, Q2 financial results could be underwhelming due to lower revenues (especially in the Air Pollution Control segment), and I think that this could be a good time for investors to trim or close their positions as the share price is near $1.40.

Investor takeaway

Fuel Tech booked significant revenue growth in Q1 2023, but it seems that the company executed mainly low-margin projects during the period as the gross margin fell to just 38.5%. For comparison, the gross margin achieved in 2021 was 49%. I’m concerned that Fuel Tech will stay in the red over the remainder of 2023 and it looks like Q2 could be challenging as the order backlog fell to $7.59 million as of March. I’m cutting my price target on Fuel Tech to $1.40 and considering the stock is hovering near that level, my rating is now neutral.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.