KanawatTH/iStock via Getty Images

Dear Fellow Shareholders,

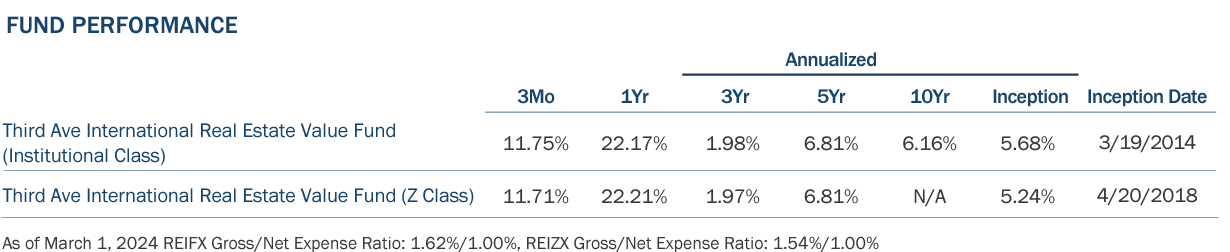

We are pleased to provide you with the Third Avenue International Real Estate Value Fund’s (the “Fund”) report for the quarter ended September 30, 2024. During the period, the Fund generated a return of +11.75% (after fees) compared to the most relevant benchmark, the FTSE/EPRA NAREIT Global ex U.S. Index[1] (the “Index”), which returned +16.74% for the same period. Over the past year, the Fund generated a return of +22.17% (after fees) versus +23.29% (before fees) for the Index.

Activity And Observations

During the quarter, a broad recovery in public international real estate resulted from an easing in monetary conditions, including interest rate cuts and improving credit spreads. Furthermore, toward the end of the quarter, China’s announcement of monetary easing and some fiscal ‘stimulus’ boosted Asian equities. While the share price rally over the quarter helped to reduce some of the discounts, the index would still need to increase by more than 30% to get back to pre-COVID valuations, as shown in the following chart.

*US Real Estate is Green Streets Market Cap weighted net asset value estimates for their coverage of the US REIT sector. The International Real Estate Index is a composite constructed by TAM. The index takes the regional average weights over the last 15 years. Price to book data is from each regional index. For Japanese Real Estate Investment Trusts, Daiwa Research data is used, and for Japanese real estate companies an average of the three largest companies price to book value including unrealized gains is used.

Although the Fund has trended in line with the index so far this year, the Fund’s returns trailed the benchmark during the most recent quarter for a few reasons: (i) currency, which was responsible for about half of the divergence and mostly related to the appreciation in the Japanese yen, to which the fund has significantly less exposure; (ii) political uncertainty, especially surrounding Mexican and U.S. elections resulting in weak relative returns from the Fund’s Mexican nearshoring-exposed industrial real estate investments; and (iii) a lack of resource conversion[4], as the Fund has not benefitted from a significant takeover event so far this year.

While outsized currency moves can be expected occasionally, Fund Management remains comfortable with no exposure to Japanese Real Estate Investment Trusts given their low yields, lack of growth prospects, and external management structures. Instead, Fund Management prefers a smaller allocation to Real Estate Operating Companies that retain their cash flow, can reinvest in the business, and are free to redevelop and develop real estate, manage external assets, and recycle capital, providing an ability to create value. Regarding Mexico, strong industrial fundamentals remain in place, and entities such as the Fund’s investment in Vesta appear deeply mispriced, trading at a 10% implied cap rate and 30% below net asset value by Fund Management’s estimates.

Further, resource conversions such as privatizations, mergers, and spin-outs have significantly contributed to the Fund’s excess returns over its 10+ year history. Although there have not been any significant developments on this front so far this year, we believe merger and acquisition (M&A) activity will likely increase in the coming periods alongside declining interest rates and increasing liquidity. Higher public market values also seem as if they will support pent-up demand on the buy and sell side from real estate private equity firms.

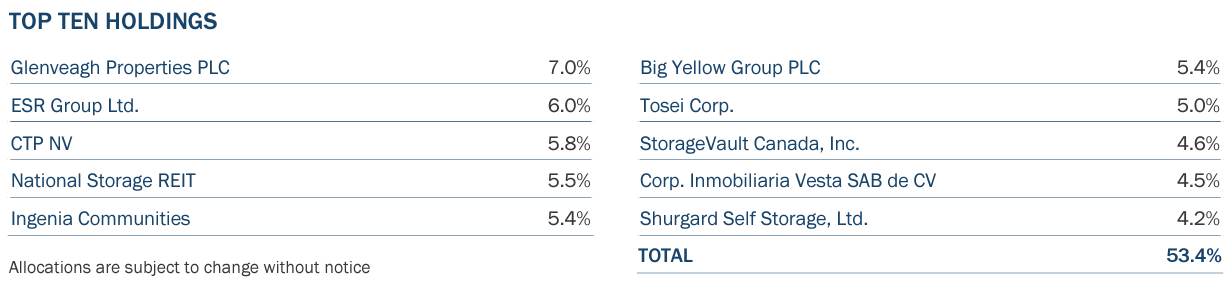

In this regard, Fund Management closely tracks the potential privatization of ESR Group (OTC:ESRCF) (“ESR”), a pan-Asia logistics and data center manager and developer held by the Fund. As mentioned in last quarter’s letter, a consortium of U.S. private equity groups led by Starwood Capital has made an indicative proposal. Post-quarter end, ESR announced an updated proposal from an expanded consortium, which included an arm of Qatar Investment Authority, Warburg Pincus, and ESR’s founders. Fund Management believes that any successful proposal would need to be made at a significant premium to the current share price.

Furthermore, Fund Management was not surprised to see the Spanish financial press (Cinco Dias, 11 Sep 2024) comment on the possibility of the Fund’s investment in Spanish homebuilder Aedas Homes (“Aedas”) being a potential resource conversion candidate. A U.S. private equity group (Castlelake) has a controlling stake in Aedas and was responsible for establishing the homebuilder out of the ashes of Spain’s housing market crash following the great financial crisis. If, indeed, Castlelake wishes to exit Aedas, there are three likely methods: (i) an outright privatization, (ii) a merger with another listed homebuilder and a staged sell-down of the stake, (iii) a large secondary offering of shares. All three could prove positive for shares, particularly given that Aedas has been historically difficult for larger Funds to invest in, given the more concentrated shareholder base.

Staying in Spain, the Fund re-initiated an investment position in Spanish diversified REIT Merlin Properties (OTCPK:MRPRF)(“Merlin”) during the quarter. Merlin owns a portfolio of office, retail, and logistics assets across Spain and Portugal, with a combined portfolio valued at US$13 billion. Fund Management has closely followed Merlin since its initial public offering in 2014, and has generally been impressed with management’s strategic ability to (i) scale a quality asset base through portfolio acquisitions, (ii) remain focused on its geographic region of expertise, (iii) build a preeminent Spanish logistics portfolio, and (iv) add value by redeveloping office and retail assets through the cycle. Perhaps fortuitously, Merlin also sold a significant portfolio of single-tenant bank branches representing around 15% of the company in early 2022, enabling Merlin to reduce debt levels at peak asset prices just before the negative impact of interest rate rises was felt.

With a better-capitalized balance sheet, Merlin has successfully developed three data center properties in Madrid, Barcelona, and Bilbao. These assets are 90% pre-committed and have a capacity of 60 megawatts (“mW”). Impressively, this US$600mn investment should deliver a net yield on cost exceeding 10%. Recognizing the potential to add value through data center development, Merlin has built up an additional US$2.3 billion pipeline to build an additional 200 mW, underwritten with similar attractive yields and returns.

Spain and Portugal have some desirable factors for data center development: power is available and relatively inexpensive, ‘green’ energy share is high, adequate land is available, and a location on the western edge of Europe means significant digital traffic passes through the region. Additionally, the international data center development cycle is many years behind the U.S., with Europe having less than 40% of the installed capacity per capita. As such, Fund Management considers Spain and Portugal uniquely positioned to take advantage of the data center real estate cycle.

Recognizing the opportunity in data center development, during the quarter, Merlin raised meaningful equity capital to help fund the pipeline. As a result, Merlin’s data center development plans are somewhat de-risked as equity funding is in place, the land is owned, and the power and much of the building ‘permits’ are secured or well progressed.

Despite Merlin’s significant data center pipeline and well-capitalized development plans, the current share price reflects none of this upside potential, and the stock is trading at a discount to book value. For value investors, this represents a compelling entry point, aligning with Third Avenue’s core philosophy of identifying undervalued, well-managed assets poised for long-term outperformance. In the meantime, shareholders benefit from Merlin’s large and diversified real estate portfolio, generating attractive cash flow.

Merlin complements the Fund’s investment in Hong Kong data center operator Sunevision Holdings Ltd. (“Sunevision”). A subsidiary of listed real estate group Sun Hung Kai Properties, Sunevision is the leading data center owner and operator in Hong Kong. The company’s data centers have impressive connectivity and are particularly well-positioned to take advantage of attractive data center fundamentals across Asia, where accelerated cloud adoption, Artificial Intelligence (“AI”) deployments, and enterprise digitalization are driving demand.

Given the scarcity of developable land in Hong Kong, the market’s ability to deliver new high quality data center supply is constrained. Sunevision, however, has been working on developing a substantial data center since 2018. The first phase of this development, which increases the size of Sunevision’s portfolio by 50%, is now open, with most of it leased or committed, which will drive significant earnings growth over the next few years. In addition, a further project phase in the same development will almost double the size of Sunevision’s portfolio. Importantly, power, land, and entitlements are secured with base building works completed so that the multi-level project can be delivered in a shortened period with reduced risk.

Currently, Sunevision trades at less than half our conservative estimate of the value of its real estate (measured by net asset value) and undemanding earnings multiple of less than 10x; none of this growth is factored into the current share price. Moreover, this growth trajectory cannot be matched by the large U.S. data center Real Estate Investment Trusts, which trade at much higher (expensive) multiples.

In a positive for the Asian region and companies like Sunevision, at the end of the quarter, the central Chinese government unveiled monetary easing and some initial fiscal stimulus. The jury is out on the stimulus’s eventual impact on the real economy. However, initially, the positive impacts are felt with a rapid rally in Chinese equities and, to a lesser extent, Hong Kong-listed equities. The stimulus suggests Beijing is now focused on strengthening consumption battered by a residential property market downturn and an egregious period of COVID lockdowns. Fund Management believes this positive impact should eventually be felt in cities like Singapore.

The city-state of Singapore has roots as a trading port dating back to the British Empire, and similar to Hong Kong, it too benefits from a legal system based on English common law. Today, Singapore has one of the highest gross domestic products[6] per capita globally (higher than the U.S.), with its free and open economy benefiting from its geographic location on the Straits of Malacca, with the largest transshipment hub in the world linking east to west via the Indian and Pacific oceans. Singapore acts as a gateway to many major growth economies, and its finance sector is well advanced, with the city increasingly acting as a crucial asset management hub for the entire Asian region. Combined with limited land, all these factors screen positively for real estate investors such as Fund Management. One of the asset types that are most likely to benefit from any improvement in the Chinese consumer is lodging and entertainment, given that Singapore and China recently agreed to Visa-free travel resulting in a significant increase in incoming Chinese tourism.

With this in mind, the Fund initiated an investment position in Genting Singapore (OTCPK:GIGNF)(“Genting”), the owner and operator of Resort World Sentosa, an integrated resort opened in 2010. This property comprises over 120 acres of land and offers 1,600 hotel rooms, a 160k square foot casino, and several family-friendly theme parks such as Universal Studios and aquariums. The casino is one of only two currently allowed in Singapore, with exclusive rights at a minimum through 2030. Fund Management has followed Genting closely for several years, with Third Avenue’s Value Fund holding a position since 2021.

There are several positive considerations, including (i) Genting’s balance sheet has no debt and significant cash (35% of market cap), (ii) ample land means Genting Singapore can expand the resort and has plans for a significant 700-room luxury hotel and other attractions, (iii) in Fund Management’s opinion the casino ‘duopoly’ will likely last well beyond 2030, (iv) tourism arrivals are not yet back at peak pre-COVID levels and should continue to improve over the next few years, and (v) Resorts World Sentosa is not solely reliant on the Chinese consumer as resort benefits from Singapore’s high tourist arrivals from Indonesia, India, and Malaysia in addition to Singaporean locals.

Regarding valuation, Genting’s shares seem mispriced in an absolute and relative sense, trading at attractive multiples and a meaningful discount to our estimate of net asset value and the historical cost of developing the resort. Notably, Genting’s most similar peer is U.S.-listed Las Vegas Sands (“Sands”), which has exposure to five casinos in Macau and controls the other Singaporean integrated resort, Marina Bay Sands. Despite many similarities, Sands trades at about 13x trailing earnings before interest, taxes, depreciation, and amortization[5], whereas Genting trades at only 6x.

Positioning

Following the addition of Genting, the Fund’s Asian exposure now represents 33% of its assets, with the Fund maintaining a diverse exposure to geographic regions, as shown below.

* Third Avenue International Real Estate Value Geographic exposure at 9/30/2024 Regional exposure reflects where the company is listed.

Regarding asset types, industrial/logistics, residential, and self-storage real estate asset types continue to make up the majority (69%) of the Fund’s exposure. Following the Genting investment, the Fund’s lodging/resorts exposure is now 7% of Fund assets, and with the addition of Merlin, the Fund has a 5% exposure to data centers.

Given this exposure to individual property asset types in a focused geographic footprint, they tend to have smaller portfolios of assets. As shown below, they are often characterized as small-and mid-market-cap companies.

Fund Commentary

The attractive valuation discounts apparent in investments such as Sunevision and Genting are common across listed real estate in Asia. In our view, this is not only due to public markets participants implying significant discounts to the underlying real estate value, but they also do not seem to factor in upside potential such as accretive developments or improving fundamentals. Third Avenue founder Marty Whitman often described such a setup as one where the only real “downside” was in the discounting widening further. Provided the issuer is both well-managed and well-capitalized, that is. This phenomenon is restricted not only to Asia but also to Western markets, as is the case with Merlin. One area in Western markets where we believe markets are inefficiently pricing the current value of underlying real estate and its significant upside potential is self-storage, for which the Fund has a 20% exposure.

As discussed in previous quarterly shareholder letters, self-storage real estate is relatively immature outside the U.S. as an asset class. There is also less supply as measured by lower square footage per capita and difficulty delivering new supply in many international cities. In addition, the demand picture is benefitting as consumer awareness improves, and ongoing urbanization and declining home sizes make storage more desirable.

This long-term opportunity is not reflected in current share prices, in our opinion, with the Fund’s self-storage investments trading on average at 15%-20% discounts to Fund Management’s conservative estimates of real estate value (net asset value). This compares to the more mature U.S. market where self-storage Real Estate Investment Trusts trade at significant premiums of about 15-20%.

When considering the industry’s immaturity and portfolios with more recent development completions and acquisitions, on average, the occupancy of the Fund’s international self-storage investments is low, averaging about 81%, compared to the U.S. which is above 90%. Conservatively, if international self-storage were to be leased up to 90% as the portfolios mature, the Fund’s investments should benefit from significant earnings upside given the fixed-cost nature of the facilities. Additionally, the Fund’s self-storage investments have large and accretive development pipelines. In aggregate, Fund Management estimates between 30% and 40% upside to earnings based on lease-up and development that does not exist anywhere near to the same degree in U.S. self-storage Real Estate Investment Trusts. Over time, this upside should be reflected in share prices. However, a near-term catalyst is an uptick in housing market activity.

Like the U.S., subdued housing market activity caused by higher interest rates or the “rate lock” phenomenon has tempered demand fundamentals for self-storage real estate. That said, international self-storage has proven much more resilient, with some declines in occupancy more than offset by rental increases. The Fund’s self-storage investments are also concentrated in housing markets where floating-rate mortgages predominate (Australia) or fixed mortgage terms are short (Canada, UK). Therefore, declining interest rates are likely to transmit into consumer income and housing market activity reasonably quickly. Any uptick in housing market activity should positively impact self-storage occupancy and income levels, acting as a catalyst for the Fund’s self-storage investments.

Fund Management’s insight piece provides further thoughts regarding some of the unique demand and supply drivers in international real estate, such as the self-storage asset type. Fund Management hopes this commentary makes clear that in addition to diversification benefits for many portfolios, real estate companies listed outside of the U.S. currently offer attractive valuation and growth characteristics, as well as the opportunity for active managers to benefit from inefficient pricing with a lack of competition.

We thank you for your continued support and look forward to writing to you again next quarter. In the meantime, please don’t hesitate to contact us with any questions or comments atrealestate@thirdave.com.

Sincerely,

Quentin Velleley, CFA Portfolio Manager

|

Past performance is no guarantee of future results; returns include reinvestment of all distributions. Past performance and current performance may be lower or higher than performance quoted above. Investment return and principal value fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. For the most recent month-end performance, please visit the Fund’s website at www.thirdave.com. The Advisor has contractually agreed, for a period of one year from the date of the Prospectus, dated March 1, 2024, to waive advisory fees and/or reimburse Fund expenses in order to limit Net Annual Fund Operating Expenses (exclusive of taxes, interest, brokerage commissions, acquired fund fees and expenses, dividend and interest expense on short sales and extraordinary expenses) to 1.00% of the average daily net assets of the Institutional Class and Z Class (the “Expense Limitation Agreement”). The Expense Limitation Agreement may be terminated only by the Board of Trustees of Third Avenue Trust. If fee waivers had not been made, returns would have been lower than reported. Past performance is no guarantee of future results; returns include reinvestment of all distributions. The chart represents past performance and current performance may be lower or higher than performance quoted above. Investment return and principal value fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. For the most recent month-end performance, please call 1-800-673-0550. The fund’s investment objectives, risks, charges, and expenses must be considered carefully before investing. The prospectus contains this and other important information about the investment company, and it may be obtained by calling 800-443-1021 or visiting www.thirdave.com. Read it carefully before investing. Distributor of Third Avenue Funds: Foreside Fund Services, LLC. Third Avenue offers multiple investment solutions with unique exposures and return profiles. Our core strategies are currently available through ’40Act mutual funds and customized accounts. Important Information This publication does not constitute an offer or solicitation of any transaction in any securities. Any recommendation contained herein may not be suitable for all investors. Information contained in this publication has been obtained from sources we believe to be reliable, but cannot be guaranteed. The information in this portfolio manager letter represents the opinions of the portfolio manager(s) and is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed are those of the portfolio manager(s) and may differ from those of other portfolio managers or of the firm as a whole. Also, please note that any discussion of the Fund’s holdings, the Fund’s performance, and the portfolio manager(s) views are as of September 30, 2024 (except as otherwise stated), and are subject to change without notice. Certain information contained in this letter constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue” or “believe,” or the negatives thereof (such as “may not,” “should not,” “are not expected to,” etc.) or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual performance of any fund may differ materially from those reflected or contemplated in any such forward-looking statement. Current performance results may be lower or higher than performance numbers quoted in certain letters to shareholders. Date of first use of portfolio manager commentary: October 15, 2024 FUND RISKS: In addition to general market conditions, the value of the Fund will be affected by the strength of the real estate markets. Factors that could affect the value of the Fund’s holdings include the following: overbuilding and increased competition, increases in property taxes and operating expenses, declines in the value of real estate, lack of availability of equity and debt financing to refinance maturing debt, vacancies due to economic conditions and tenant bankruptcies, losses due to costs resulting from environmental contamination and its related clean-up, changes in interest rates, changes in zoning laws, casualty or condemnation losses, variations in rental income, changes in neighborhood values, and functional obsolescence and appeal of properties to tenants. The Fund will concentrate its investments in real estate companies and other publicly traded companies whose asset base is primarily real estate. As such, the Fund will be subject to risks similar to those associated with the direct ownership of real estate including those noted above under “Real Estate Risk.” Foreign securities from a particular country or region may be subject to currency fluctuations and controls, or adverse political, social, economic or other developments that are unique to that particular country or region. Therefore, the prices of foreign securities in particular countries or regions may, at times, move in a different direction than those of U.S. securities. Emerging market countries can generally have economic structures that are less diverse and mature, and political systems that are less stable, than those of developed countries, and, as a result, the securities markets of emerging markets countries can be more volatile than more developed markets may be. Recent statements by U.S. securities and accounting regulatory agencies have expressed concern regarding information access and audit quality regarding issuers in China and other emerging market countries, which could present heightened risks associated with investments in these markets. The Adviser’s use of its ESG framework could cause it to perform differently compared to funds that do not have such a policy. The criteria related to this ESG framework may result in the Fund’s forgoing opportunities to buy certain securities when it might otherwise be advantageous to do so, or selling securities for ESG reasons when it might be otherwise disadvantageous for it to do so. For a full disclosure of principal investment risks, please refer to the Fund’s Prospectus. 1 FTSE EPRA Nareit Global ex US Index is designed to track the performance of listed real estate companies and Real Estate Investment Trusts in both developed and emerging markets. By making the index constituents free-float adjusted, liquidity, size and revenue screened, the series is suitable for use as the basis for investment products, such as derivatives and Exchange-Traded Funds (ETFs). It is not possible to invest directly in an index. 2 Excess Return refers to the return from an investment above the benchmark. Source: Investopedia 3 Price to Book Ratio: A company’s price-to-book ratio is the company’s current stock price per share divided by its book value per share (BVPS). This shows the market valuation of a company compared to its book value. 4 Resource conversions include mergers, privatizations, spin-outs, recapitalizations or significant buybacks. 5 EBITDA, short for earnings before interest, taxes, depreciation, and amortization, is an alternate measure of profitability to net income. 6 Gross domestic product (GDP) is the total monetary or market value of all the finished goods and services produced within a country’s borders in a specific time period. 7 Small Cap is Equity Market Cap up to US$2bn, Mid Cap US$2bn-US$10bn, Large Cap >US$10bn. Past performance is no guarantee of future results. |

{kind=link}

{kind=link}

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.