Arf & Wag Studio/iStock via Getty Images

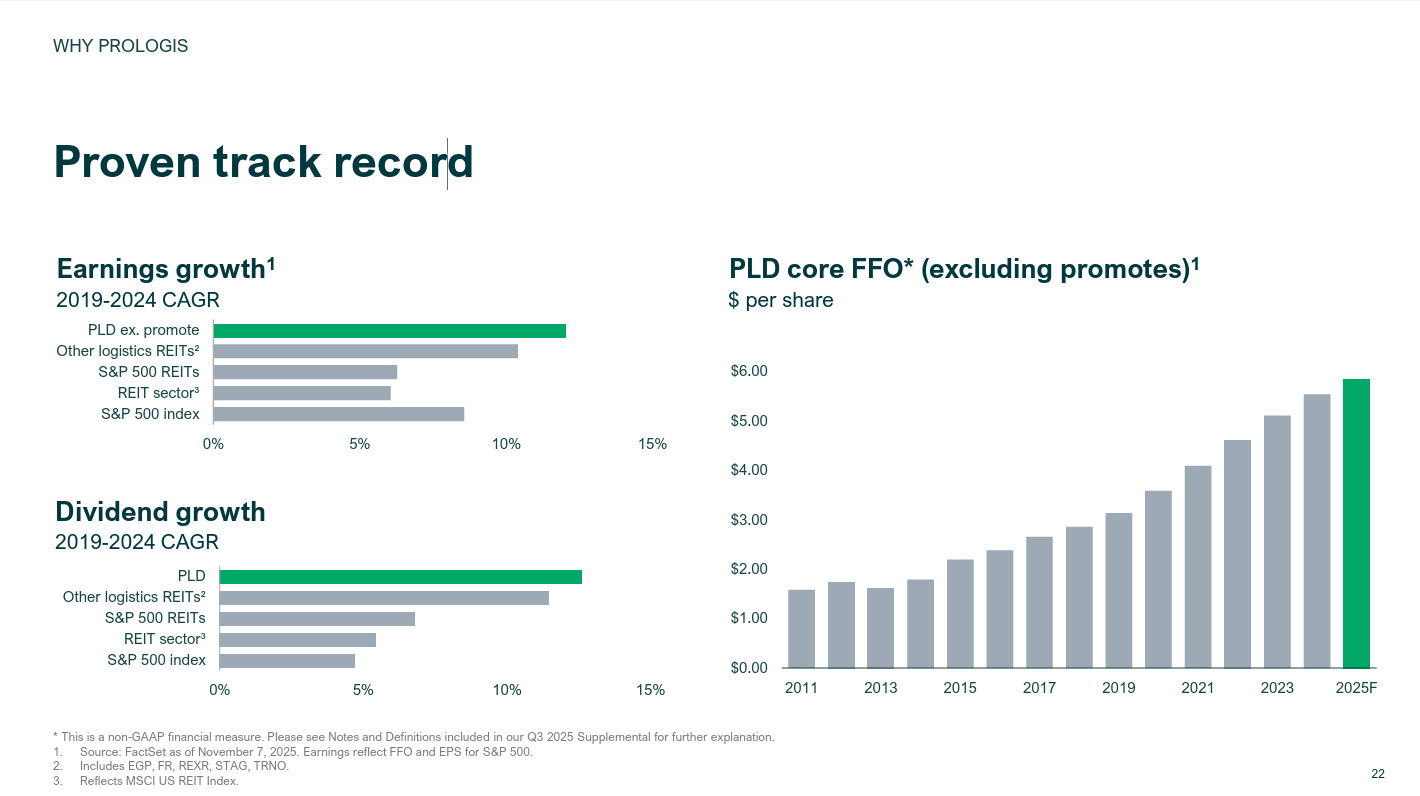

Prologis (PLD) delivered another strong quarter, continuing a consistent trend despite the macro noise. PLD is a large industrial REIT with a 1.3 billion square foot portfolio and $215 billion in assets under management. In terms of pure size, the company is a behemoth.

I last published a PLD article to Seeking Alpha in 2022. At the time, the stock had fallen in price substantially. Recently, the stock price has been on an upward trajectory.

FFO & AFFO

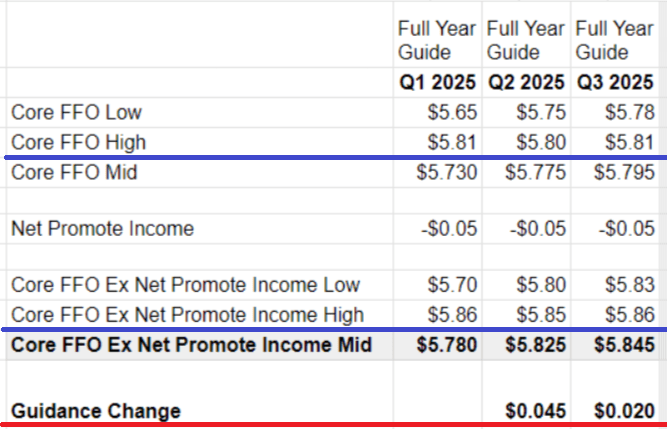

PLD had a solid quarter for Core FFO and beat consensus estimates. Their AFFO came in below estimates, but AFFO is usually very volatile for PLD, which I will explain later in this article.

As you can see on the following slide, PLD lists their Core FFO excluding “promotes”:

{kind=link}

We like to track the company’s Core FFO ex Net Promote Income because it gives a cleaner picture of how the company is performing:

{kind=link}

It is important to know that “Net Promote Income” is normally a positive number. This is a rare year when it has come in as a negative. It also has an extreme amount of volatility from quarter to quarter.

What is Net Promote Income?

What is “Net Promote Income”? That’s a good question. For investors who aren’t familiar with this term, “Net Promote Income” is the promote revenue earned from third-party investors during the period (net of stock compensation, taxes, foreign currency derivative gains and losses, etc.). Said another way, Prologis has several joint ventures. It’s a large part of their strategic capital business. When those ventures outperform, PLD earns promote income. The number can go negative, which is what happened this quarter.

Management provides the “Core FFO excluding promotes” figure so investors can see the operational performance without getting thrown off by a line item that is inherently extremely volatile. That being said, it’s an important number to account for – especially long term.

NOI & Earnings

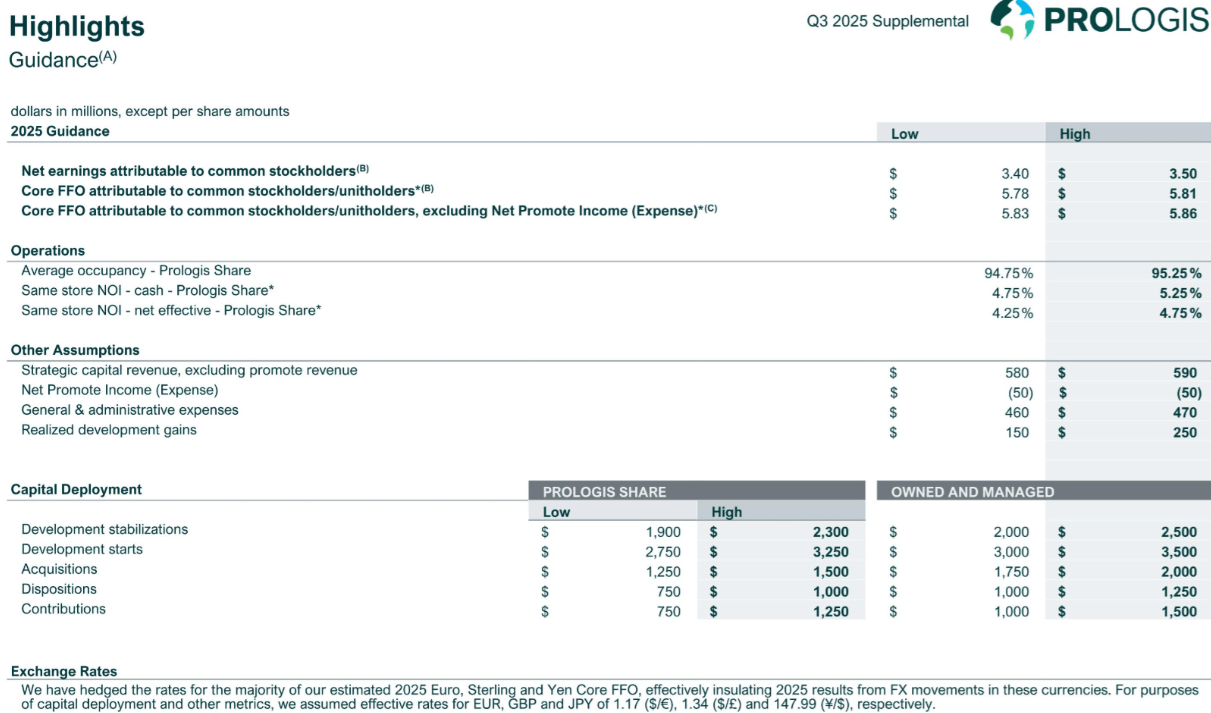

Prologis increased their guidance for both same-store NOI metrics by 50 basis points:

{kind=link}

If we annualize the Q3 same-store NOI growth, it comes out to roughly $27 million in cash Net Operating Income and $30 million in net effective Net Operating Income.

This was a solid quarter on the NOI front, especially considering how large the portfolio is. When a company is this massive, investors shouldn’t expect big swings. What investors should be looking for is consistent and repeatable growth. Prologis continues to deliver both.

PLD stated that strong rent change is expected to support NOI growth going forward. Tenants are willing to pay higher rents for PLD’s locations. The leasing spread will flow through into future NOI.

Management nudged their full-year guidance higher. These small upward changes tell investors that the company remains stable and management is comfortable looking forward.

Prologis is sending a clear message this quarter: fundamentals are healthy and trending slightly better than previously thought.

Development

Development continues to be one of PLD’s competitive advantages. Below are two quotes from their CFO, Timothy Arndt, on the Q3 earnings call:

In terms of capital deployment, we had a lighter quarter of development starts with expectations for a strong fourth quarter due to the specific timing of transactions. 2/3 of our volume in the fourth quarter – in the third quarter – was in build-to-suits with large global customers, many of whom rank in our top 25. We signed an additional 9 build-to-suits this quarter, driving the total to 21 so far for the year and amounting to $1.6 billion of total expected investment.

In capital deployment, we are increasing development starts at our share to a new range of $2.75 billion to $3.25 billion. And as a reminder, only previously announced data center starts are included in this guidance. We are also increasing our combined disposition and contribution guidance by $500 million to a range of $1.5 billion to $2.25 billion at our share.

Prologis doesn’t need to buy properties at questionable cap rates. They can just build high-quality assets at superior yields and lock in the demand from tenants early. Their development pipeline is one of the biggest reasons the company consistently performs well.

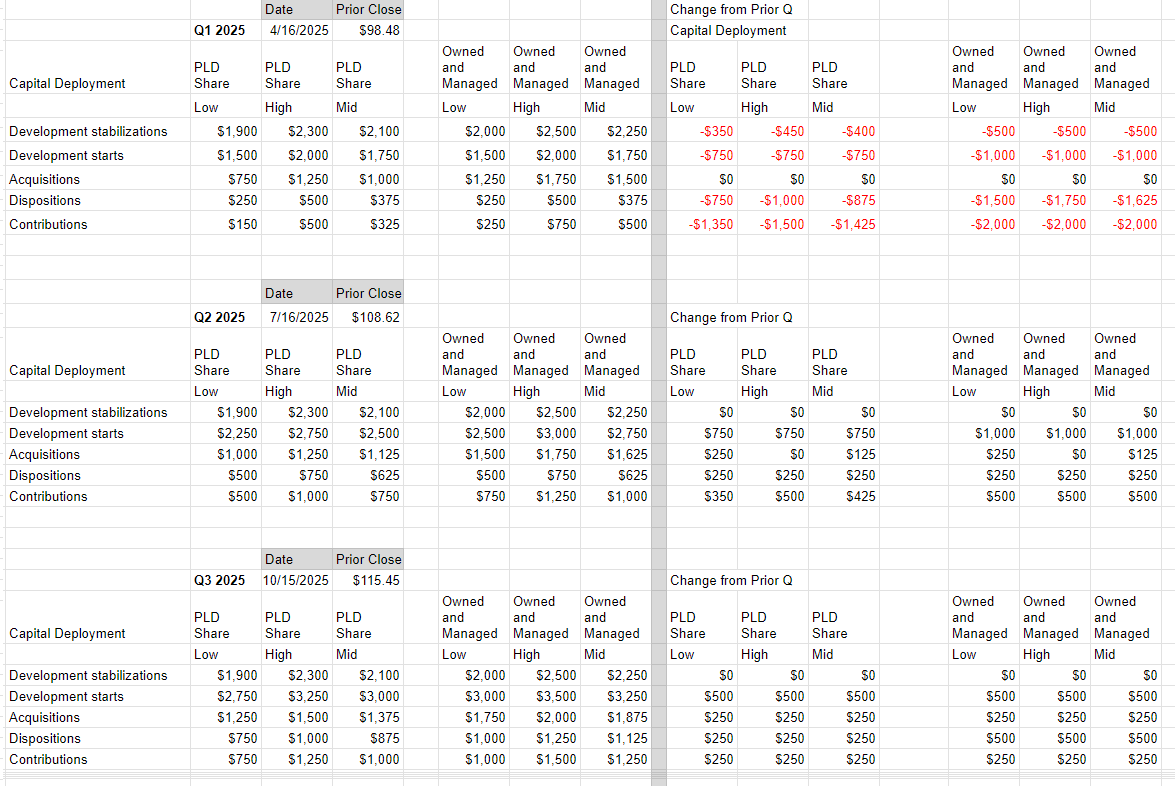

I created a table showing PLD’s plans to deploy their capital based on multiple earnings releases. Apologies to anyone confused by the graphic, but it’s what I built personally, and I thought it was worth sharing with readers:

{kind=link}

Final Thoughts

PLD continues to show why it sits at the top of the industrial REIT sector. The company delivered another strong quarter with healthy NOI growth, a meaningful guidance bump, and solid leasing spreads. Even in the current macro environment, the demand for PLD’s infill properties remains strong.

The promote income volatility can make quarter-to-quarter comparisons tricky. However, the core operations continue to trend in the right direction. When you strip out all the noise, PLD’s earnings are still increasing. The long-term growth story is there – one of the biggest development pipelines in the industry.

Prologis is one of the largest REITs when it comes to market cap. It continues to win through consistency, scale, and intelligent capital allocation. Add this quarter to the list of accomplishments. For long-term investors who want exposure to a high-quality industrial REIT, PLD remains one of the stronger options in the sector.