JHVEPhoto

Illumina (NASDAQ:ILMN) is a San Diego, California-based life sciences and biotechnology company, with operations spanning over 155 countries. The firm manufactures and markets integrated systems for genome sequencing and biological function testing.

Illumina 41st Annual J.P. Morgan Healthcare Conference Presentation

{kind=link}

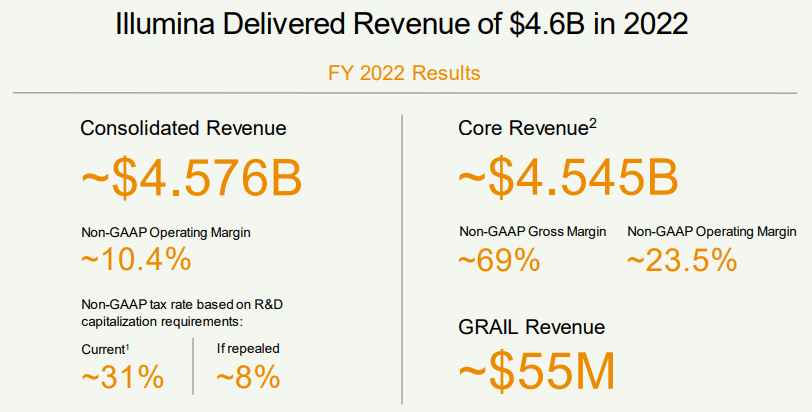

In the previous year, these activities have enabled revenues of $4.58bn and a non-GAAP operating margin of 10.4%.

Introduction

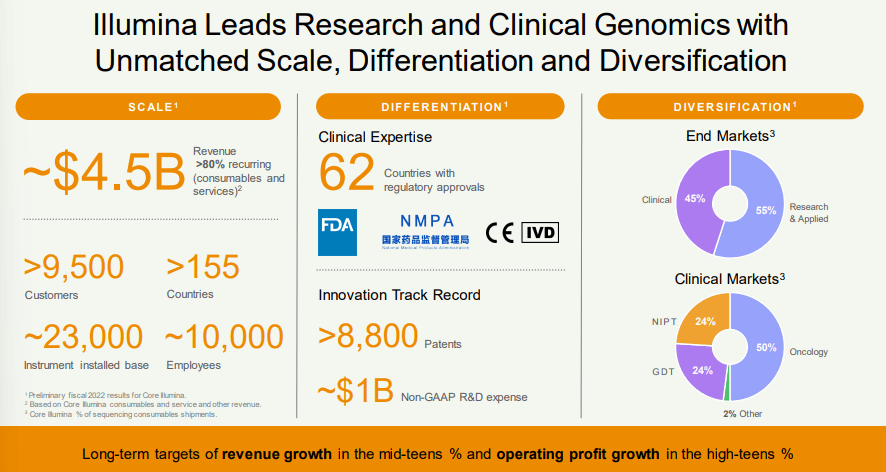

The principal aim of Illumina remains scale growth above all else. Evidenced jointly by poor net income figures and the company’s overall operational presence, Illumina successfully maintains over 9500 customers and an installed base of 23,000 instruments. As such, Illumina sustains a capability to navigate complex international regulatory structures throughout a diverse number of clinical and end markets.

Illumina 41st Annual J.P. Morgan Healthcare Conference Presentation

{kind=link}

The life sciences company seeks to position itself across the medical technology continuum, involved in testing, assessment, diagnosis, therapy selection, and monitoring, among others.

Illumina 41st Annual J.P. Morgan Healthcare Conference Presentation

{kind=link}

Owing to its market position, current undervaluation, and product quality, I will present a ‘buy’ case for the stock.

Valuation & Financials

General Overview

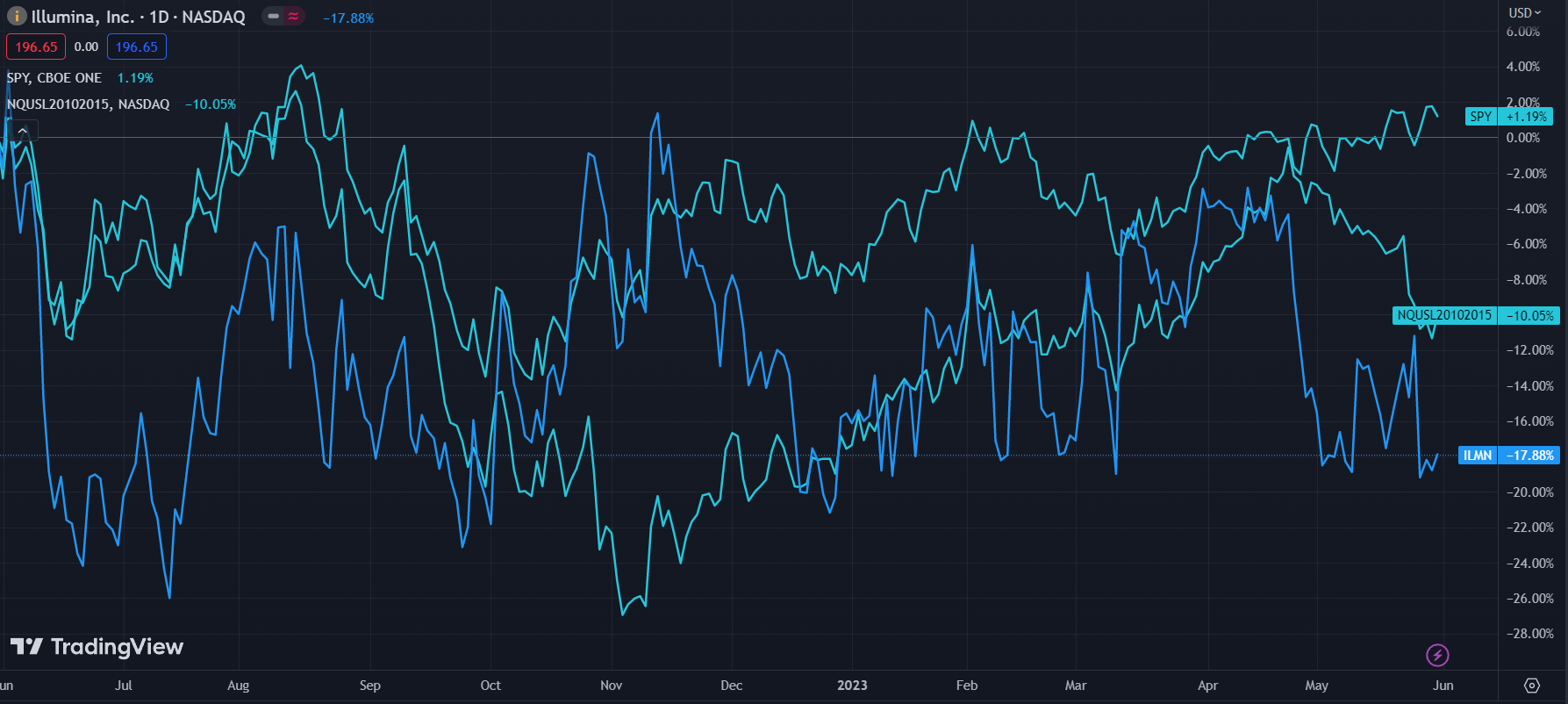

In the TTM period, Illumina- down 17.88%- has trailed both the general market, represented by the S&P 500 (SPY)- up 1.19%- and the NASDAQ US Large Cap Medical Supplies Index- down 10.05%.

Illumina (Dark Blue) vs Industry & Market (TradingView)

{kind=link}

This reflects a downtrend of healthcare stocks following reductions in healthcare investment as the effects of COVID-19 wind down. For Illumina specifically, the company has seen negative net income and free cash flow owing to temporary demand compression while seeing regulatory stress regarding the firm’s acquisition of- and order for the divestiture of- GRAIL.

Comparable Companies

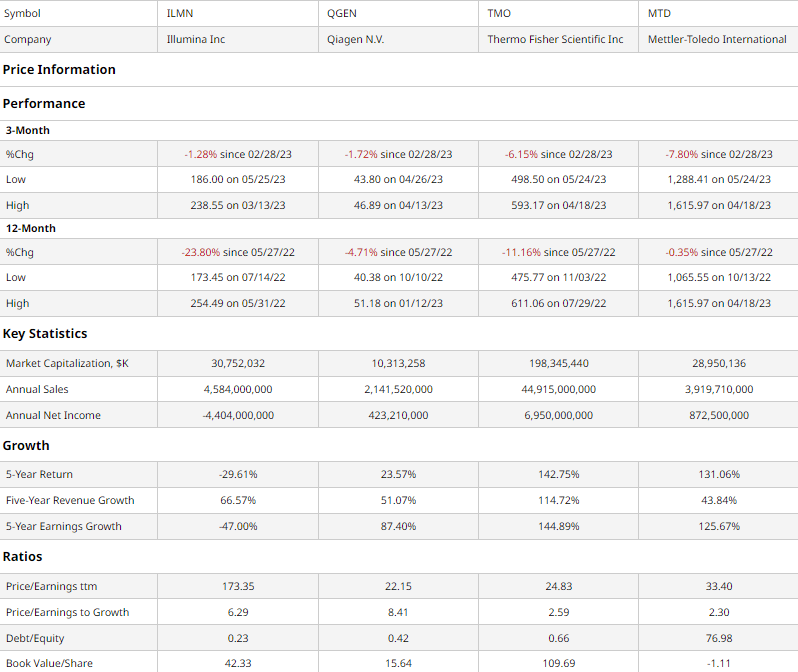

The high degree of specialization within the life sciences and biotechnology industries reduces the direct competition any single firm faces. However, either due to similar size or similar activities, the following are comparable peer companies to Illumina; Qiagen (QGEN) is a provider of sampling and assay technologies; Thermo Fisher (TMO) is among the largest medical technology firms in the world; and Mettler-Toledo (MTD) is a multinational manufacturer of laboratory equipment, similar in size to Illumina.

{kind=link}

As demonstrated above, despite delivering the best quarterly price performance, Illumina, due to both macro and individual headwinds, has experienced the poorest TTM price action.

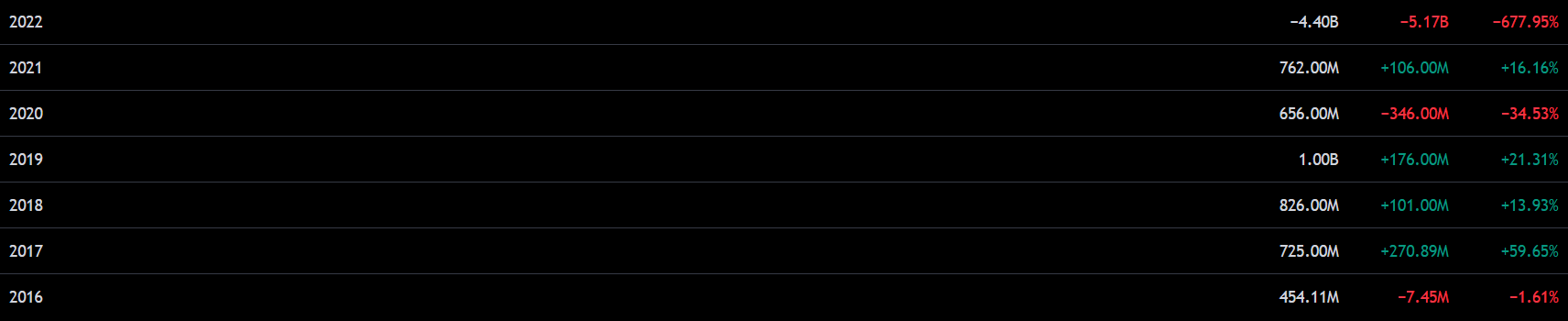

Illumina’s poor price performance is justified by poor annual net income figures, itself leading to poor multiples-based value. However, over the previous 5-years, 2022’s earnings have been an anomaly, which I do not believe will be replicated due to a significant order backlog.

Illumina Net Income Since 2016 (TradingView)

{kind=link}

Additionally, Illumina has successfully achieved significant scale growth, with the second-highest revenue growth of its peer growth. Moreover, the company maintains the lowest debt/equity ratio of the group and the second-highest BV/share.

Valuation

According to my discounted cash flow analysis, at its base case, the fair value of Illumina should be $253.94, meaning at its current price of $196.65, the stock is undervalued by 23%.

Calculated over a 5-year period without perpetuity, my DCF model assumes a discount rate of 9%, accounting for the higher equity risk premium the greater beta of the stock lends as well as the company’s low debt levels. Moreover, I assume revenue growth rates in line with historical levels smoothed out for the previous year.

AlphaSpread

AlphaSpread’s multiples-based relative valuation tool actually calculates an 8% overvaluation, projecting the fair value to be $181.11.

However, Alpha Spread’s tool fails to account for Illumina’s lower relative debt levels and contextualize the volatility of the previous year.

Leadership Across Genomics Verticals Supports Aggressive Growth

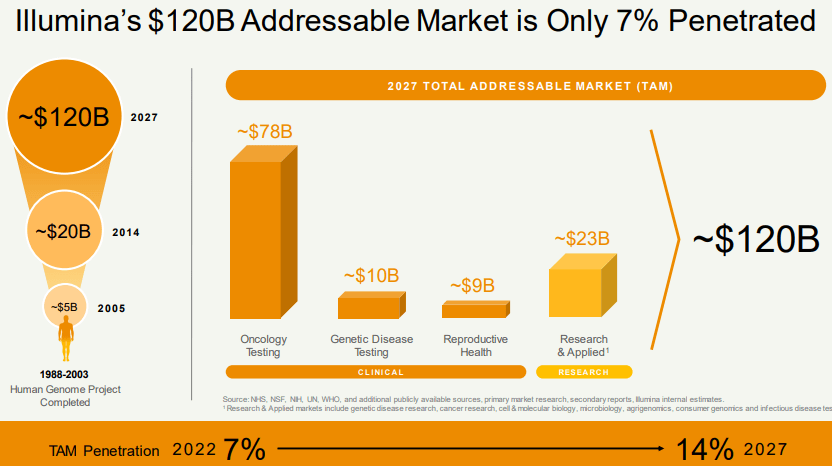

By positioning itself for scalability above all else, Illumina is targeting to expand its footprint into the $120bn TAM industries of oncology testing, genetic disease testing, reproductive health, and research and applied healthcare products. With these markets growing at a consolidated CAGR of 14.78% from 2014-2027, Illumina projects an outsized capability to capture growth. The firm’s aggressive stance is best exemplified through its $7.1bn acquisition of cancer test developer, Grail. Although the acquisition has been under considerable pressure from regulators, it nonetheless illustrates Illumina’s ambitions to penetrate these markets. Moreover, activist shareholder Carl Icahn led the replacement of board chair John Thompson with Andrew Teno, supporting the company’s capability to operate if ordered to divest from Grail.

Illumina 41st Annual J.P. Morgan Healthcare Conference Presentation

{kind=link}

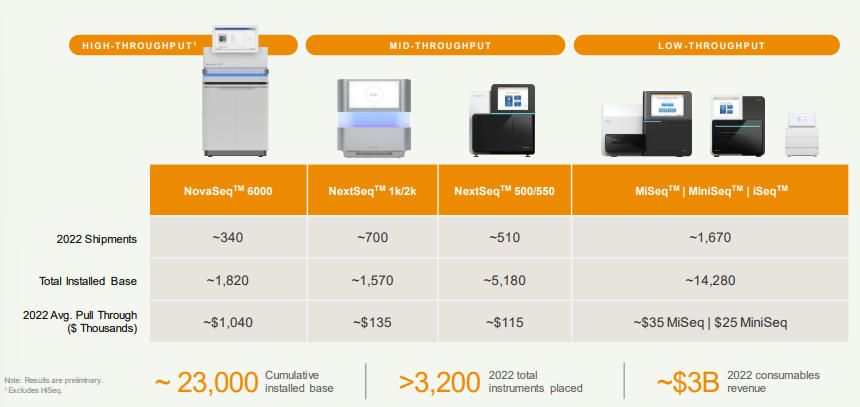

Beyond its concerted focus on scale growth, Illumina has worked towards the development of products across the genetic sequencing vertical. The company has produced products at varying price levels and with varying throughput capabilities. As such, the firm is both able to upsell given expanded client capacity and access a diversity of markets, from academic institutions to corporate clients and laboratories.

Illumina 41st Annual J.P. Morgan Healthcare Conference Presentation

{kind=link}

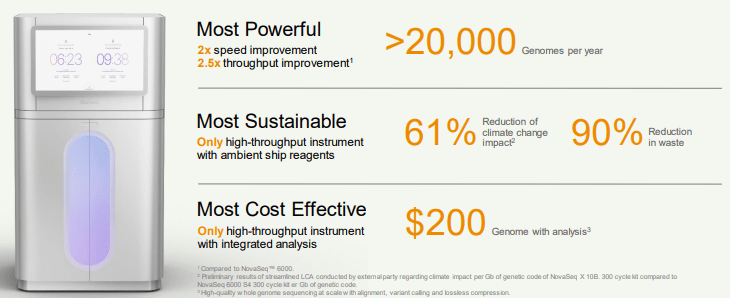

Beyond all else, Illumina’s ability to remain at the forefront of genome technologies supports its market position. With its NovaSeq X, clients can cost-effectively achieve significantly greater throughput at greater speeds. The NovaSeq X has seen the strongest pre-launch demand for any Illumina instrument yet, with over 140 orders and over 300 expected shipments for the year.

Illumina 41st Annual J.P. Morgan Healthcare Conference Presentation

{kind=link}

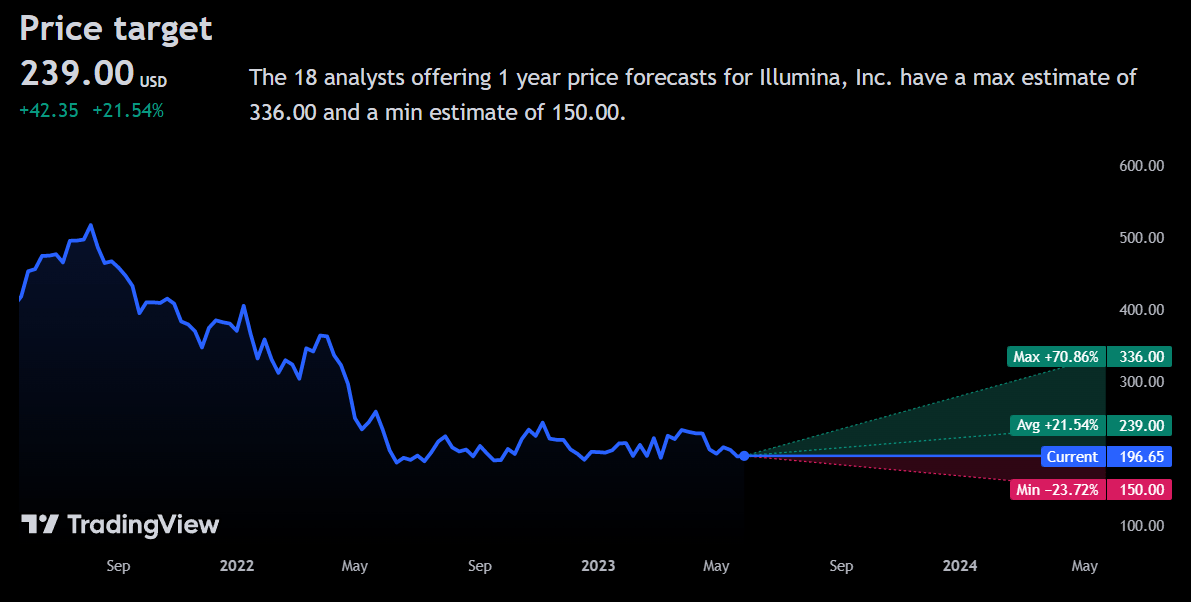

Wall Street Consensus

Analysts largely echo my positive view on the stock, estimating an average 1Y price increase of 21.54% to a price of $239.00.

{kind=link}

The minimum estimated price decline of -23.72% is largely a reflection of the general volatility of the stock, anxieties about potential divestment from Grail, and continued poor financial performance.

Risks & Challenges

Value Contingent Upon Sustained Innovation

Although Illumina continues to lead the genome sequencing market, its success and continued value is contingent upon its ability to retain its talent, protect its intellectual property and continue to innovate at this level. Failure to do so would harm the firm’s ability to generate continuous cash flows.

Dependence on Extraneous Market Demand

As demonstrated by the poor financial results of the previous fiscal year, the ability for Illumina to generate net income and cash flows is highly dependent upon demand factors; reduced demand in APAC markets, for instance, drove poor financial results in 2022. Continued demand compression, owing to interest rates or not, will lead to reduced capabilities to operate, reinvest, and grow.

Grail Divestment Risk

Although Carl Icahn’s involvement in the company is centered around his support for the divestment of Grail- thus proving Illumina’s ability to generate value despite whatever happens to Grail- selling or divesting from the firm at a loss will harm the company’s financial position, market position, and potentially lead to reductions in the value of the stock.

Conclusion

In the short term, I expect Illumina to revert from the poor financial results of the previous year.

In the long term, I project Illumina will be well-positioned to leverage growth trends across the life sciences and biotechnology markets.