Kirpal Kooner

Dear readers,

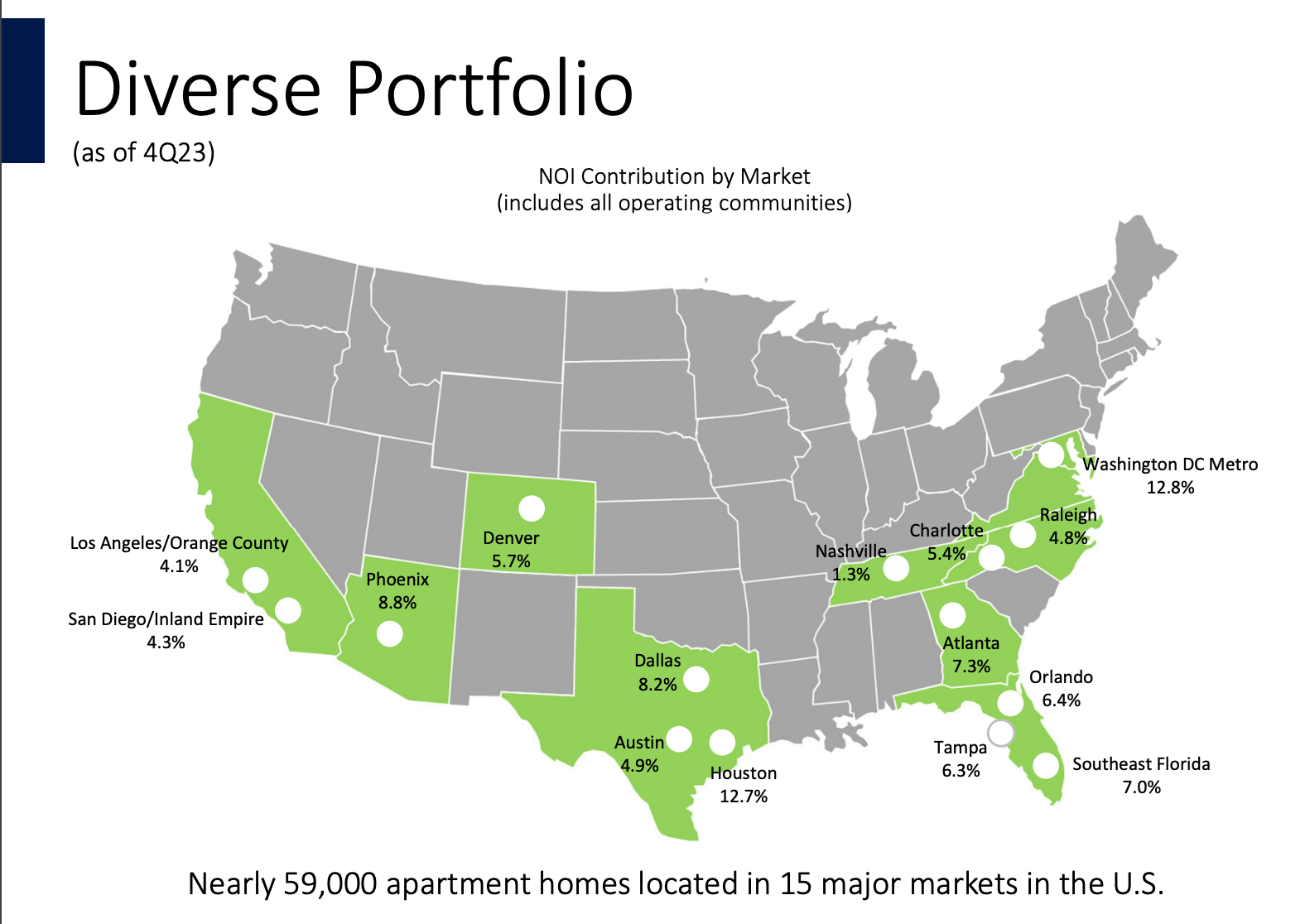

Camden Property Trust (NYSE:CPT) is a major apartment REIT with nearly 60,000 units located across the Sunbelt (including California). Notably, a large portion of units are low-rise (59%) and B-Class (62%) which brings a number of advantages. I’ve written extensively about why I see B-Class in the Sunbelt as well positioned, especially relative to A-Class. If you’re interested, you can read up on this topic in my article on BSR REIT (OTCPK:BSRTF) titled BSR REIT: Why B-Class Apartments Could Outperform.

{kind=link}

I’ve covered Camden before, last February, and came to a conclusion that the stock was a BUY at $120 per share. My thesis, which called for an OKish 9% total return, was based on CPT’s impressive A- rating and a valuation of 18x FFO and an implied cap rate of 5.5%. I was well aware of the over-supply risk in Camden’s markets, spent a considerable part of my last article on the expected supply-demand dynamics, and came to a conclusion that the record supply in 2024 and 2025 (especially in Texas) was likely to get (mostly) absorbed.

It turned out, however, that I was wrong. Sunbelt apartment markets have softened and as a result, my call has underperformed with an RoR of -16% compared to a stunning return of the S&P 500 (SPX) of 26%.

Market positioning

Dallas, Austin and Atlanta account for 20% of Camden’s ABR and are all amongst the top 5 cities in the U.S. with the highest expected increase in inventory in 2024. Moreover, new supply is expected to be even higher next year.

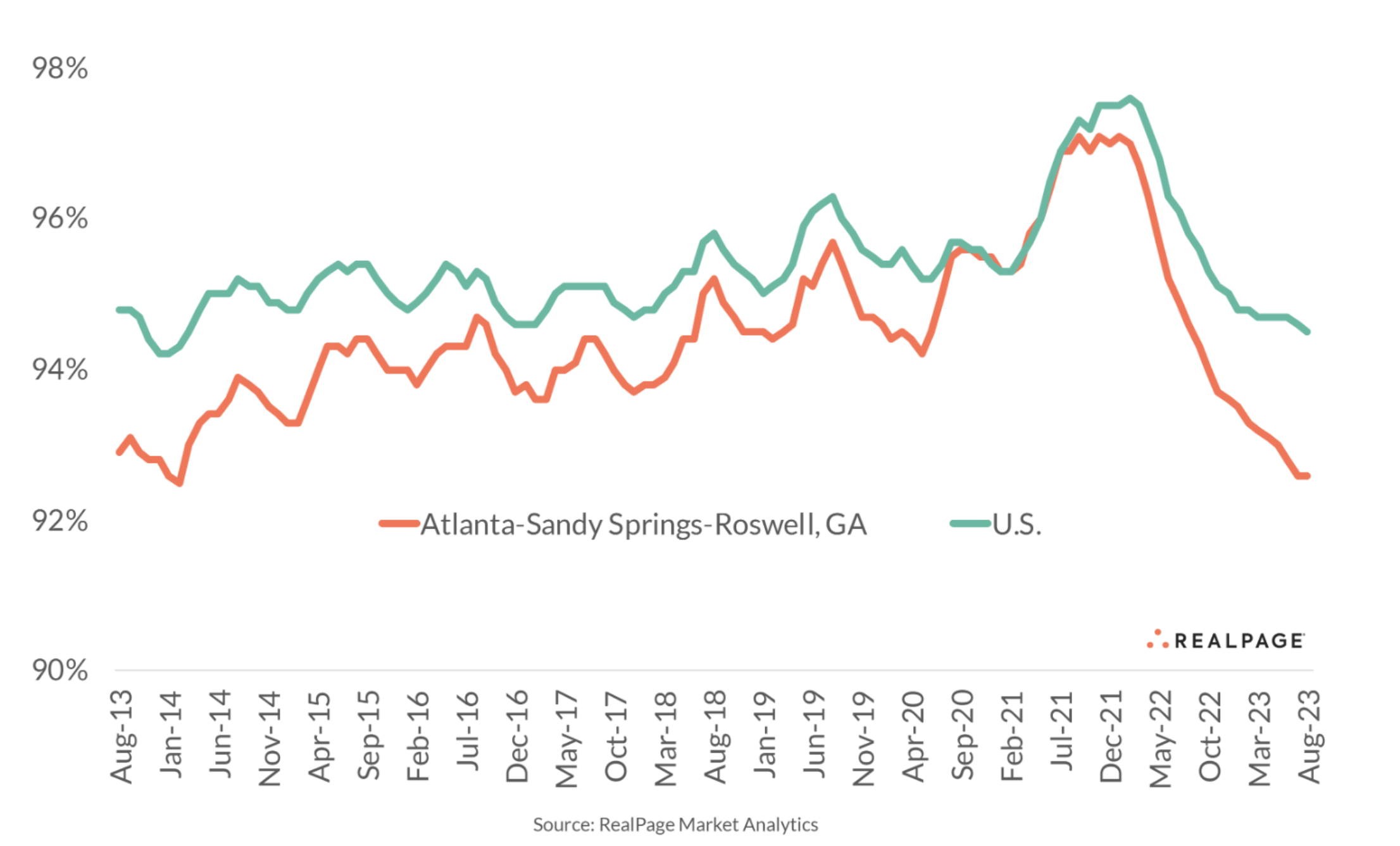

As a result, these markets are already seeing significant increases in vacancy. In Atlanta, the average vacancy increased to 8% and vacancies for new units in Dallas are as high as 10%.

{kind=link}

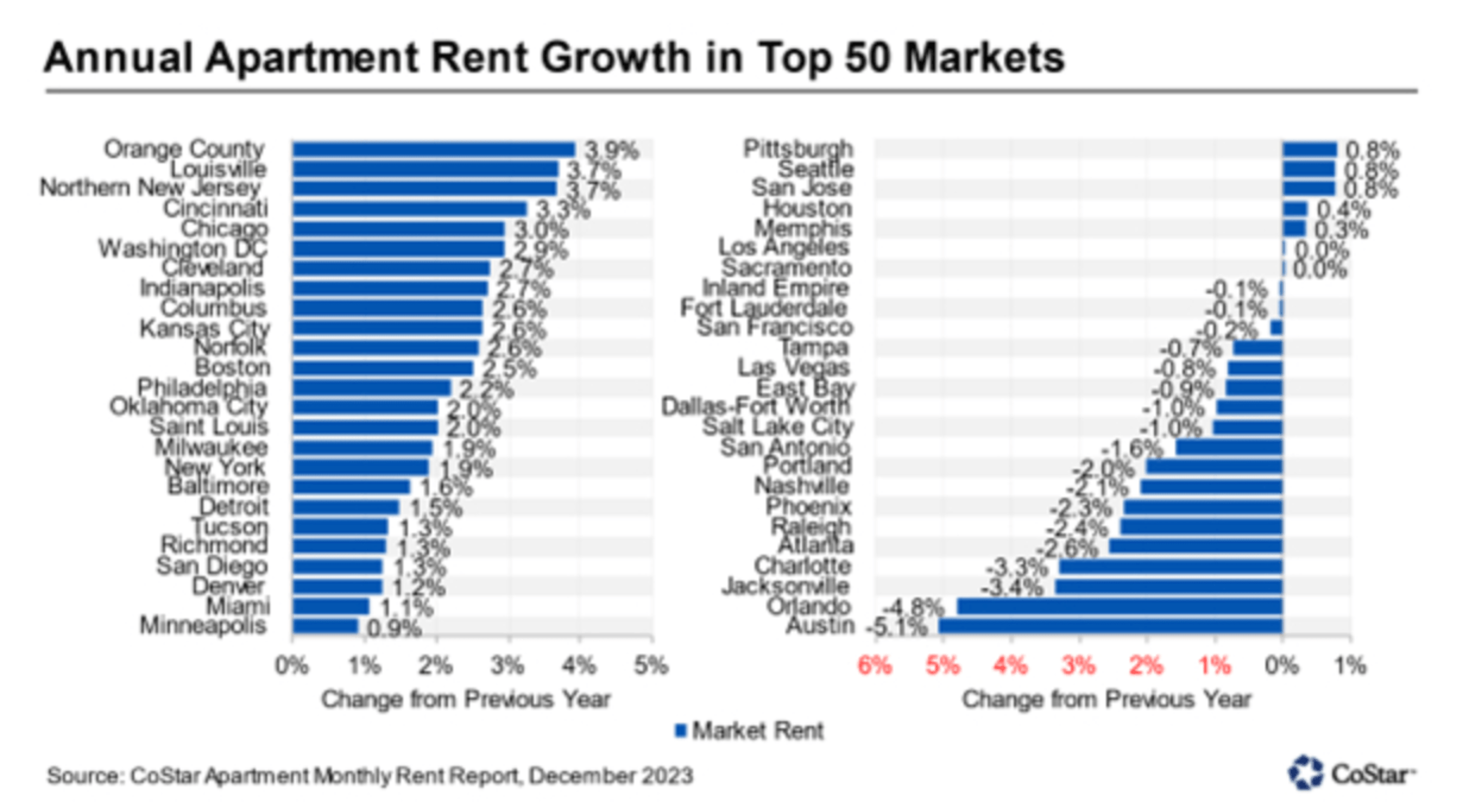

As a result, rents have come under pressure. To name a few of Camden’s largest markets, Austin is down 5.1% YoY, Orlando is down 4.6%, and Atlanta is down 2.6% YoY. And this is before the peak in supply next year.

{kind=link}

So what is the take away here?

It’s quite clear to me that rents in the Sunbelt are likely to decline further this year and in 2025. But only for A-Class space. You see, the new supply that we’ve discussed so far is entirely A-Class. B-Class doesn’t get build, rather apartments become B-Class with time as they age. As a result, Camden, which has a large portion of B-Class apartments, could be relatively resistant to declining rents. Additionally, the California exposure might actually help stabilize the portfolio, as California isn’t seeing much new supply at all and rents are expected to be steady.

In either case, I like the prospects of apartment REITs in the Sunbelt beyond 2025. Construction starts are down by 27% nation-wide over the last two years and much more in the Sunbelt as a result of rising construction, energy and financing costs. This means less supply post 2025. Combined with the ever increasing unaffordability of housing which results in more renters by necessity and therefore more demand, rents could very quickly rebound, perhaps even explode in 2025 and beyond.

Camden’s cash flow – results and guidance

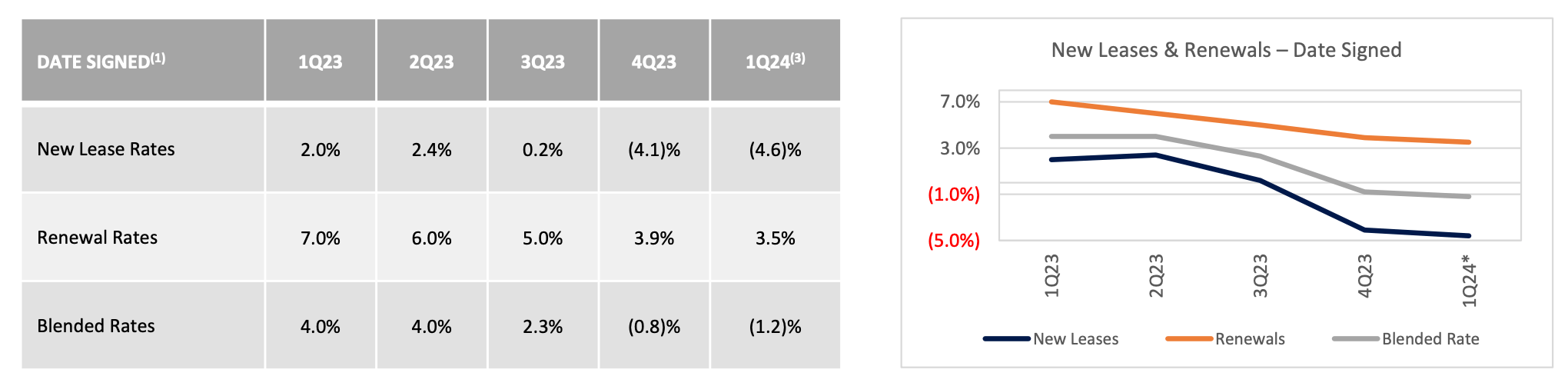

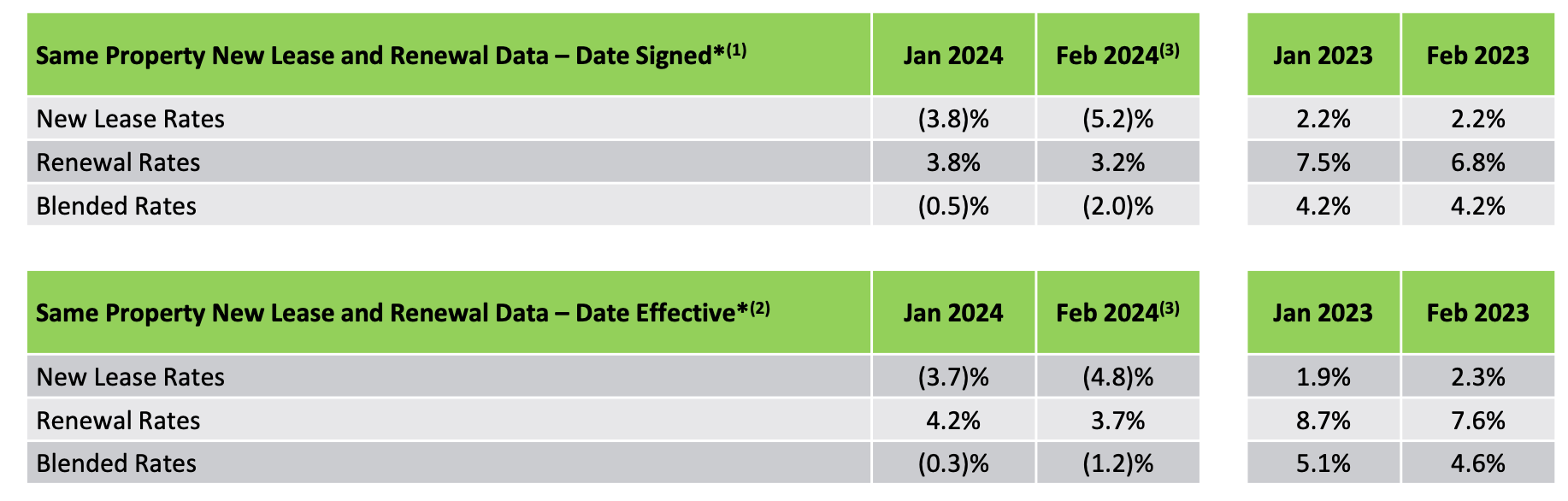

Camden managed to post solid full year 2023 results with 3% annual FFO growth. But slowing rent growth has been evident. Throughout the year, rent increases on renewals have declined from 7% in Q1 to 3.9% in Q4 and on new leases the decline has been even more pronounced as rent growth dipped into negative territory in Q4 at -4.1%.

{kind=link}

To combat this, management has implemented a marketing campaign to boost occupancy ahead of the usual peak leasing season (Q2). The campaign focuses primarily on communities with occupancy below 95% and on units that have been vacant for 30 days or more. The goal is to bring occupancy above the current 94.9%.

Going forward, management is guiding for revenue growth of 1.5% in 2024, down substantially from 2023. But rates on leases signed in January and February show that even this lower target might be hard to achieve. It is normal that leasing is slow in Q1, but a slowdown from a blended rent increase of 4-5% last year to negative 1-2% this year is hardly a positive. Notably, the slowdown has mainly been a result of around a 4% drop in rents in some of Camden’s largest and most overbuild markets such as Austin and Atlanta.

{kind=link}

As a result, management’s guidance and the general consensus for FFO growth has declined since my last article from 4-5% in 2024 and 2025 to -1.5% this year and 3% next year.

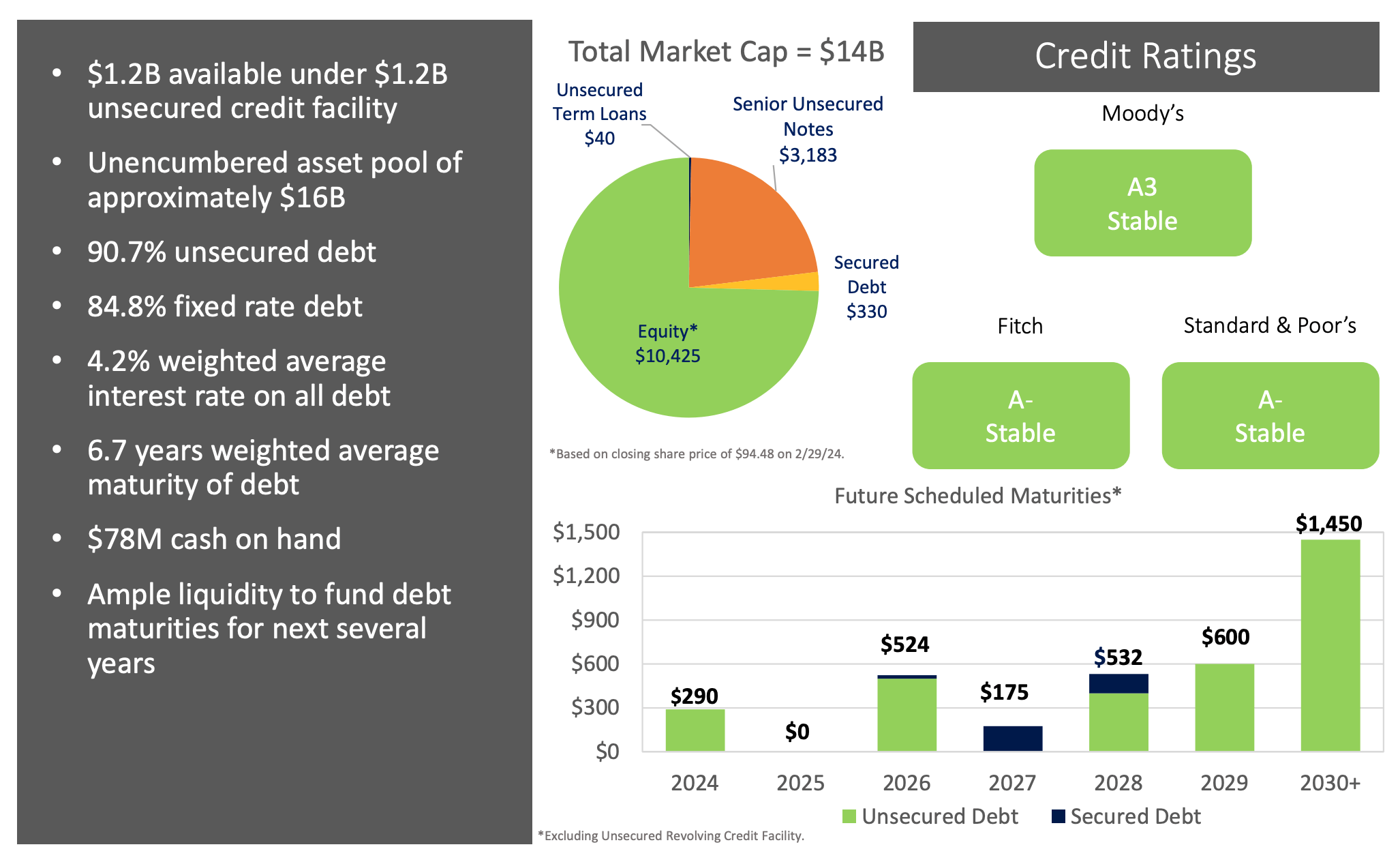

With a stable A- rated balance sheet with a large portion (85%) of fixed rate debt and low near term maturities, Camden’s cash flow (and FFO) is likely to be quite stable and predictable.

{kind=link}

Having discussed the apartment market outlook, I believe that Camden is likely to see flat FFO per share until 2025, followed by a rebound in growth post-2025, once rents increase as a result of a low supply, to around 5% per year.

But one question remains.

What is the cash flow worth?

Camden pays a 4.3% dividend yield which is very well covered with a payout ratio of just 59%. The company has a 5-year dividend growth CAGR of 5.3% which is mainly a result of steep increases in 2021 and 2022 caused by a booming Sunbelt rental market. As the market softens, however, I expect no further dividend growth this year and next year.

{kind=link}

The stock trades at 14x FFO which is fair relative to Mid-America Apartments (MAA) which trade at 15x, but have higher quality A-Class properties, and to BSR REIT which trades at 13x FOO, but focuses entirely on Texan markets that are likely to see the most new supply in the coming quarters.

The stock trades at an implied cap rate of 6.5%, which is about 190 bps above the 10-year treasury yield. While I consider the spread fair, there is certainly potential for upside if interest rates and yields decline from today’s levels.

In particular, I estimate that a drop in the 10-year yield to 4% would lead to a 25% upside and correspond to a price target of $120 per share. The math behind this is relatively simple. Using the implied cap rate formula where:

Implied cap rate = NOI / (market cap + net debt)

we can change the implied cap rate and work out a corresponding change in market cap. My assumption about the 10-year yield declining to 4% (and holding the spread of 190-200 bps constant) means that the implied cap rate would decline to about 6%. Holding NOI constant at roughly $900 Million per year, because we’re assuming little to no growth over the next two years and holding net debt constant at $3.65 Billion, we can work out that the market cap will increase by roughly 25%.

Risks

The single biggest risk to CPT’s cash flow is not rising interest rates, but rather the uncertainty regarding rents, especially in light of a high tenant turnover which tends to average 2-3 years for all apartment REITs. As (short) lease contracts expire and tenants leave, CPT’s average rent is likely to mirror market rent quite closely.

Moreover, while interest rates only have a small impact on the REIT’s cash flow, they do affect the valuation and consequently stock price a lot. As a result, a rise in interest rates or even interest rates staying elevated for longer than is now expected would most definitely result in a decline in the stock price.

Bottom Line

We’ve known for a while that supply of new A-Class apartment space in the Sunbelt would peak in 2024 and 2025. Now we’re starting to see the impact of this in the form of rising vacancies and falling rents. As a result, management has reduced its guidance and the general consensus for FFO per share growth has declined from 4-5% to zero. I expect Camden’s FFO per share to be flat until 2025, but to continue to grow by 4-5% post-2025.

While Camden cannot be considered a smoking deal at an implied cap rate of 6.5%, I do like its high credit rating, comfortably dividend and potential for upside if interest rates decline. Camden is, in essence, a relatively stable way to play interest rates while earning a solid yield. Therefore I reiterate my BUY rating here at $95 per share.