Irina Gutyryak/iStock via Getty Images

Introduction

As most of my regular readers will know, I always try to incorporate the “bigger picture” into my research, as this allows me to get a good understanding of factors that may impact the stocks in our portfolios and on our watchlist.

One of the most important things to keep in mind is the macro situation, including economic growth, interest rates, inflation, and factors like credit quality.

Leo Nelissen (Investment Framework)

{kind=link}

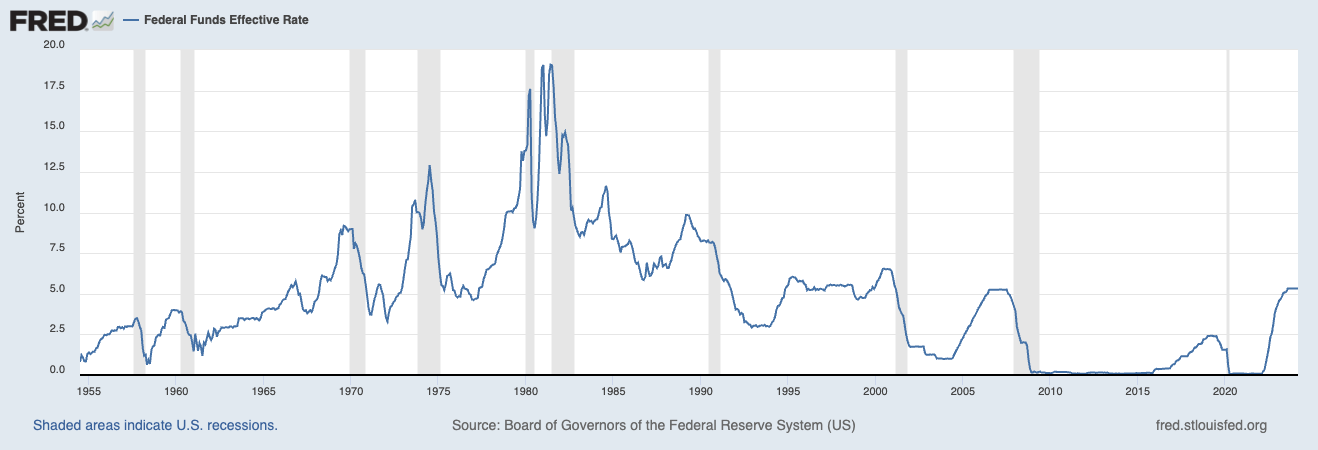

In this environment, one of the cornerstones of my research is credit quality, as I am in the camp of investors who expect both interest rates and inflation to be “higher for longer.”

Essentially, I believe that inflation will remain too elevated for the Fed to start a consistent easing cycle, potentially putting tremendous pressure on credit quality that could eventually force the Fed to pick protecting financial stability over fighting inflation.

Going back to the 1950s, the Fed had just two periods of cuts that did not see a recession – all other easing cycles came with a recession.

Federal Reserve Bank of St. Louis

{kind=link}

While every recession is different, it makes sense that aggressive hikes cause economic stress, as our developed economies are dependent on cheap debt.

Everything is fueled by debt. This includes consumer credit, mortgages, commercial debt, leases, and whatnot.

Periods of cheap debt followed by elevated rates often cause rising delinquencies that work their way through the economy. The Great Financial Crisis was one of the biggest domino effects in (modern) history.

Don’t get me wrong. I’m not making the case for another Great Financial Crisis. In this market, most banks have much stronger balance sheets, and consumer credit is much better as well.

However, we’re now in a period where tremendous stress is building on the economy. While GDP growth forecasts remain in the 2-3% range, credit quality is dropping.

Federal Reserve Bank of Atlanta

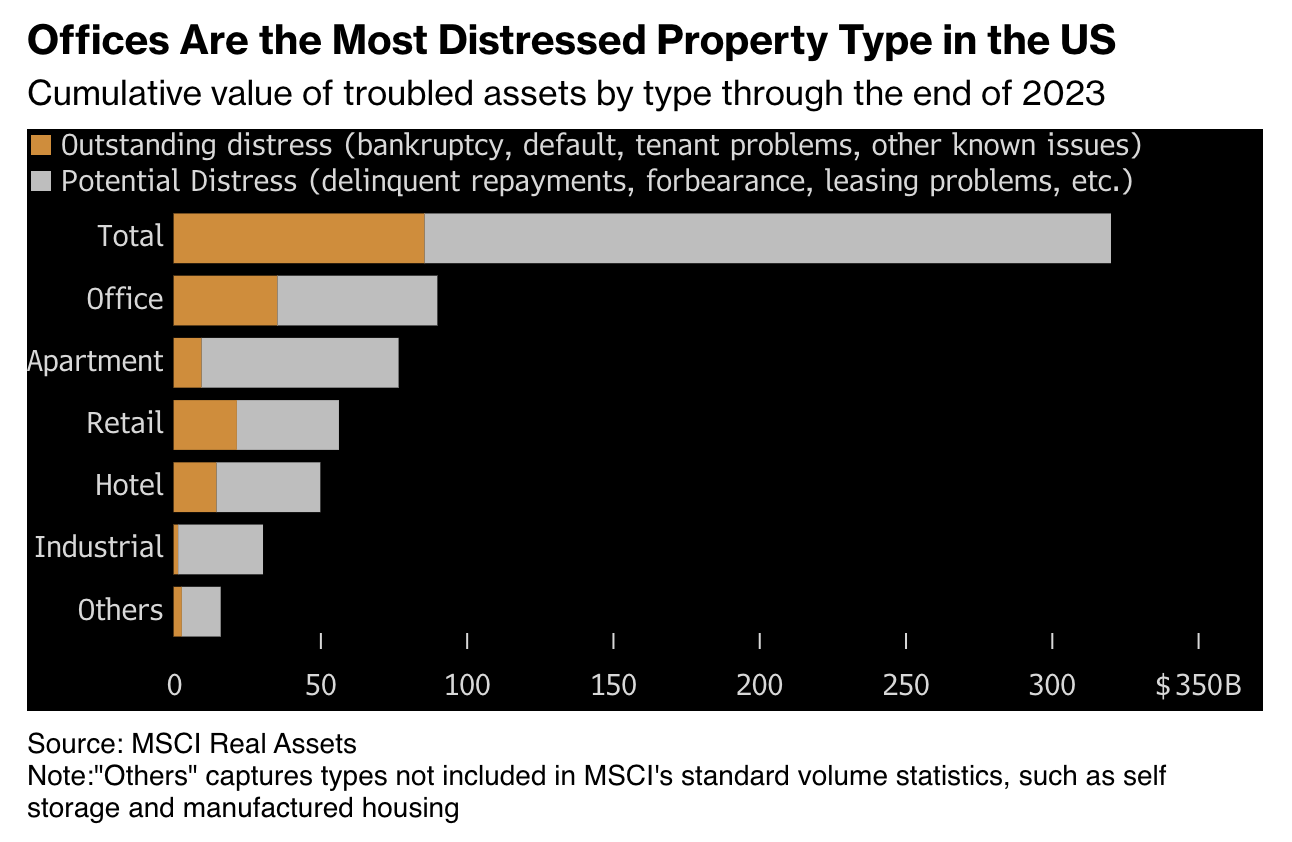

On April 3, I wrote an article on Starwood Property Trust (STWD), which I consider to be one of the best-managed commercial real estate mortgage companies.

In that article, I highlighted the rapid increase in delinquencies and at-risk debt, using the following quote from Bloomberg:

As of December, offices accounted for 41% of the value of distressed US properties, which stood at nearly $86 billion, according to MSCI. Potential distress, which refers to the erosion of an asset’s current financial standing, is at nearly $235 billion across all property types. Apartments are high on that list, with more than $67 billion in potential distress. More than 30% of that value is tied to buildings bought in the last three years, many at peak prices. – Bloomberg

{kind=link}

In other words, offices and multifamily apartments are the worst areas. Offices have been a problem since the pandemic. Now, other areas are struggling as well, as cheap financing at record prices is now meeting elevated refinancing requirements and low demand from buyers.

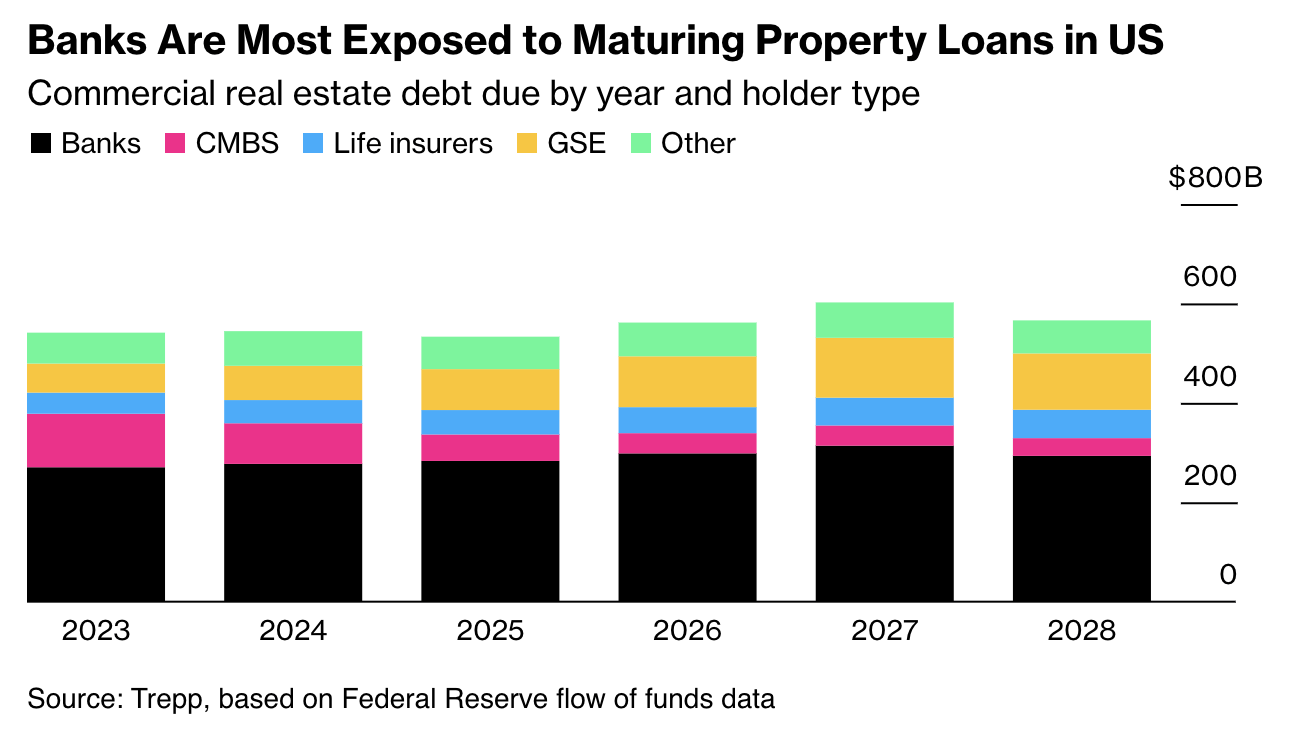

Even worse, we are now looking at more than $500 billion in annual maturities of CRE debt.

{kind=link}

Hence, at the end of March, S&P Global (SPGI) made the case that this could have severe negative consequences for lenders as it downgraded some regional banks.

Some US regional lenders could see their asset quality and performance hurt by the stresses in commercial real-estate markets, said S&P Global Ratings on Tuesday as it lowered its outlook on five lenders to negative from stable.

Increases in modified loans and loan maturities “may foreshadow a decline in asset quality and performance,” the ratings provider said in a statement. – Bloomberg

With all of this in mind, one of the lenders on my radar is the Ares Commercial Real Estate Corporation (NYSE:ACRE), the star of this article.

On November 14, I wrote my most recent article on this company, titled “14%-Yielding Areas Commercial Real Estate: We’re Beyond The Sweet Spot.”

While I made the case that ACRE is relatively resilient, I also made the case that the stock had gone beyond the “sweet spot,” meaning financial risks started to outweigh the benefits from elevated rates.

Since then, ACRE has returned -24%, including its dividend.

It also announced a dividend cut on February 22, when it lowered its dividend by 24.2% to $0.25 per share per quarter.

While it still yields 14%, I will use this article to explain why I cannot get myself to turn bullish. In fact, I’m even more worried than before, as its portfolio could see much more weakness.

So, let’s dive into the details!

Why I’m So Worried About ACRE

Before I continue, let me quickly reiterate that we’re not dealing with a poorly run company.

If ACRE were a small company with bad management, I wouldn’t even bother covering it. However, because ACRE is such a giant in its industry and a holding of many portfolios, it gives us valuable (industry) intel.

The company is a specialty finance company that primarily focuses on originating and investing in CRE loans.

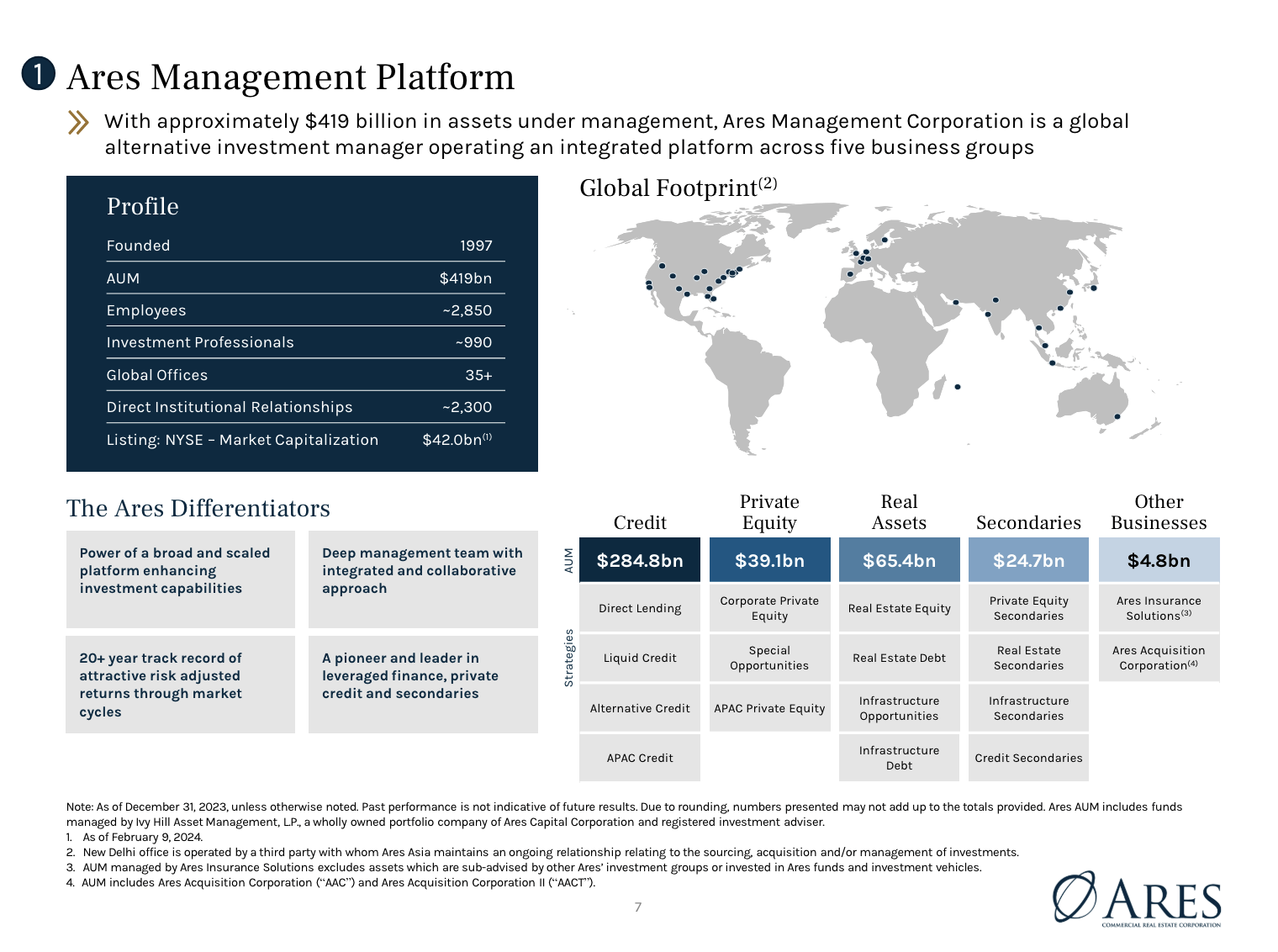

ACRE is externally managed by Ares Commercial Real Estate Management LLC, which is owned by the mighty Ares Management Corporation (ARES), a giant with more than $400 billion in assets under management and close to 1,000 investment professionals.

Ares Commercial Real Estate Corporation

{kind=link}

Essentially, the company’s strategy aims to address the financing needs of borrowers pursuing value-improving business plans on commercial real estate.

ACRE acts as a single source of financing for its customers, holding loans for investment and earning interest income.

What’s interesting is that the company believes that this macroeconomic environment is favorable. The quote below is from its 2023 10-K. I added emphasis.

In the current macroeconomic environment, many lenders are constrained by regulatory or capital requirements and increased credit losses and have de-emphasized their service and product offerings specific to commercial real estate. These factors have reduced competition and lowered overall commercial real estate transaction volume, resulting in capital providers requiring greater risk premiums for new financing commitments. – ACRE 2023 10-K

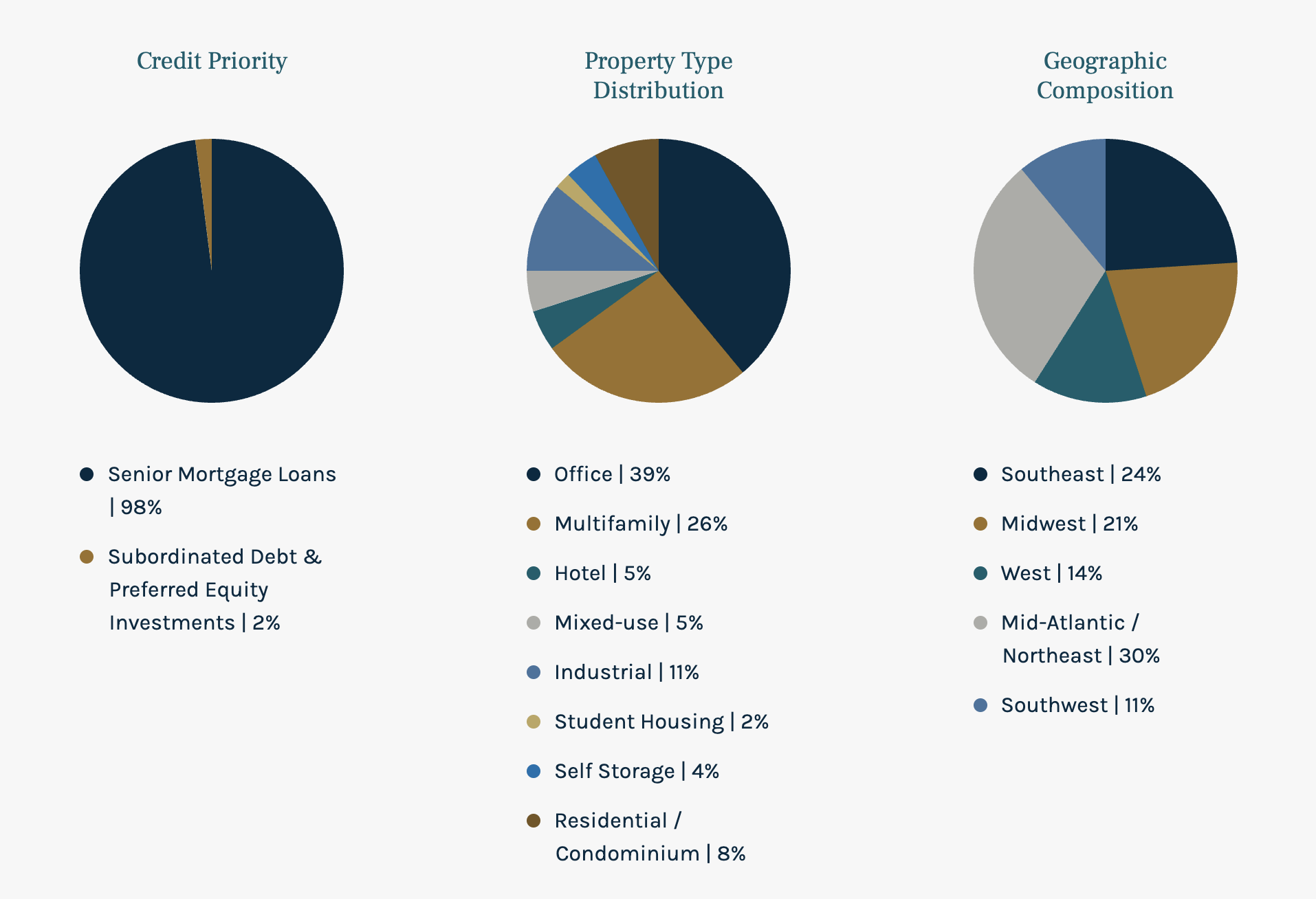

With that said, the company’s portfolio is less favorable, as it has a lot of exposure to the areas that are currently struggling: office and multifamily.

39% of its entire portfolio consists of office debt. Multifamily accounts for 26% of its exposure – that’s a combined 65%.

Ares Commercial Real Estate Corporation

{kind=link}

As a result, credit adjustments have a major impact on its financials.

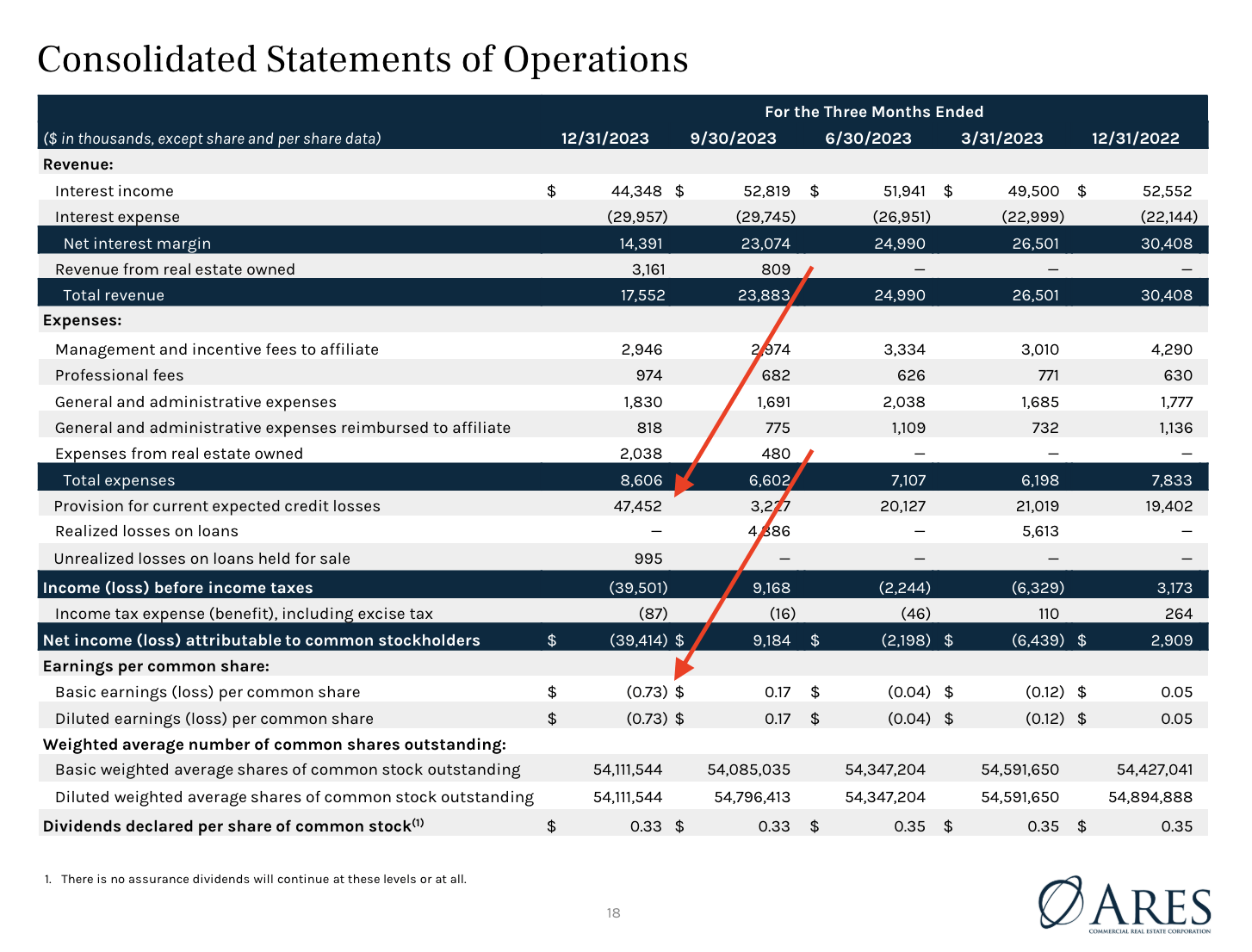

For example, the company reported a net loss of $39.4 million in the fourth quarter of 2023. This translates to a loss of $0.73 per common share.

This loss was mainly caused by a significant increase in the Current Expected Credit Loss (“CECL”) provision, which came in at $47.5 million, or $0.87 per common share.

I highlighted these numbers in the overview below.

Ares Commercial Real Estate Corporation

{kind=link}

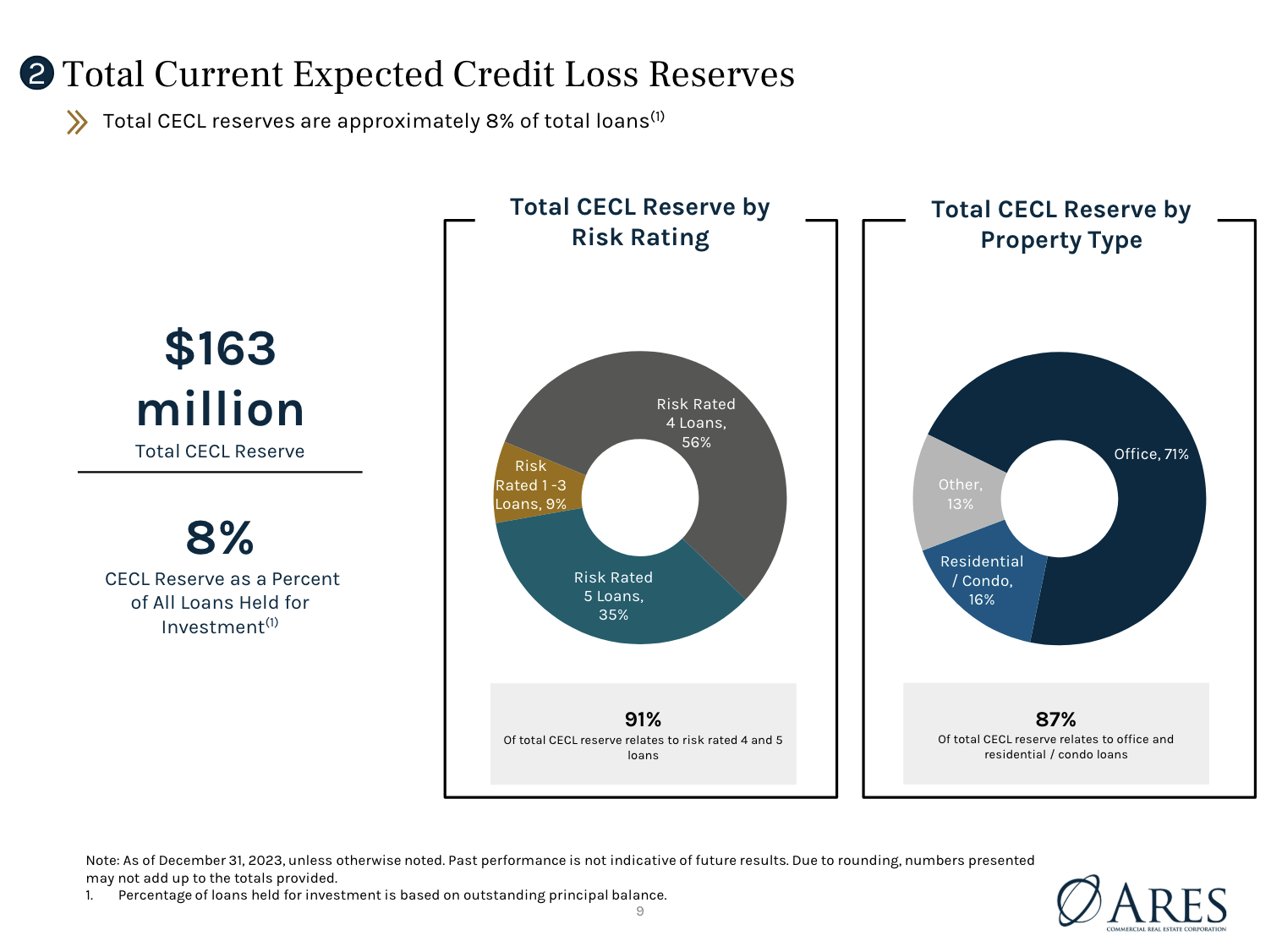

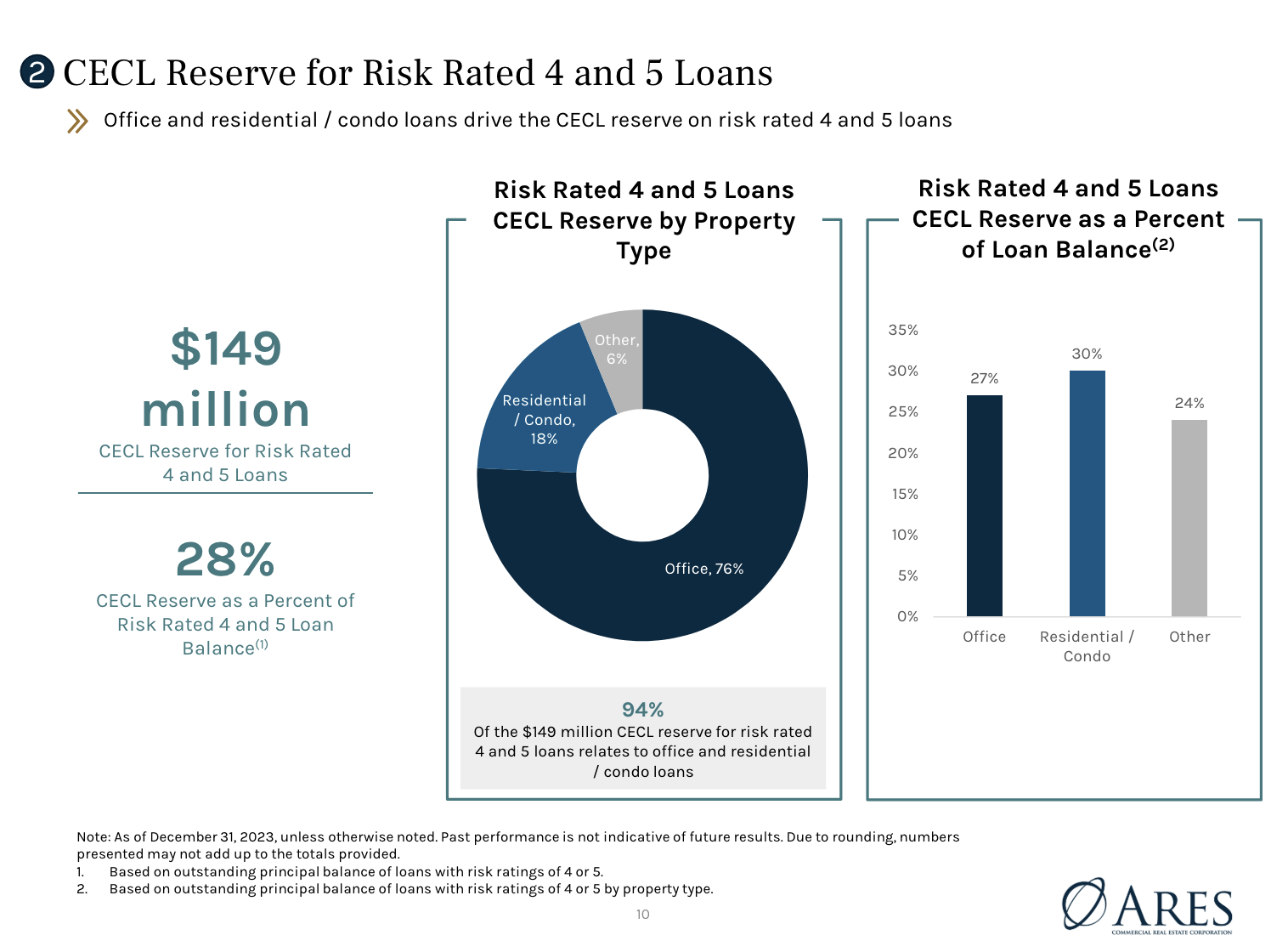

Diving into the CECL, the company increased the total CECL to $163 million by the end of 2023. This reserve represents 7.6% of the outstanding principal balance of loans held for investments.

That’s a very serious number, as it implies that the company may lose 7.6% of its portfolio to defaults!

Moreover, 91% of this reserve, totaling $149 million, applies to loans with risk ratings of four and five. Within this category, $57 million of loss reserves were allocated to three risk-rated five loans, while $92 million was assigned to six risk-rated four loans.

Moreover, office loans accounted for 71% of the total CECL, followed by residential loans (16%). This makes perfect sense in light of what we discussed in the first part of this article.

Ares Commercial Real Estate Corporation

{kind=link}

In fact, the loss reserve accounted for 28% of the balance of the four and five risk categories.

Ares Commercial Real Estate Corporation

{kind=link}

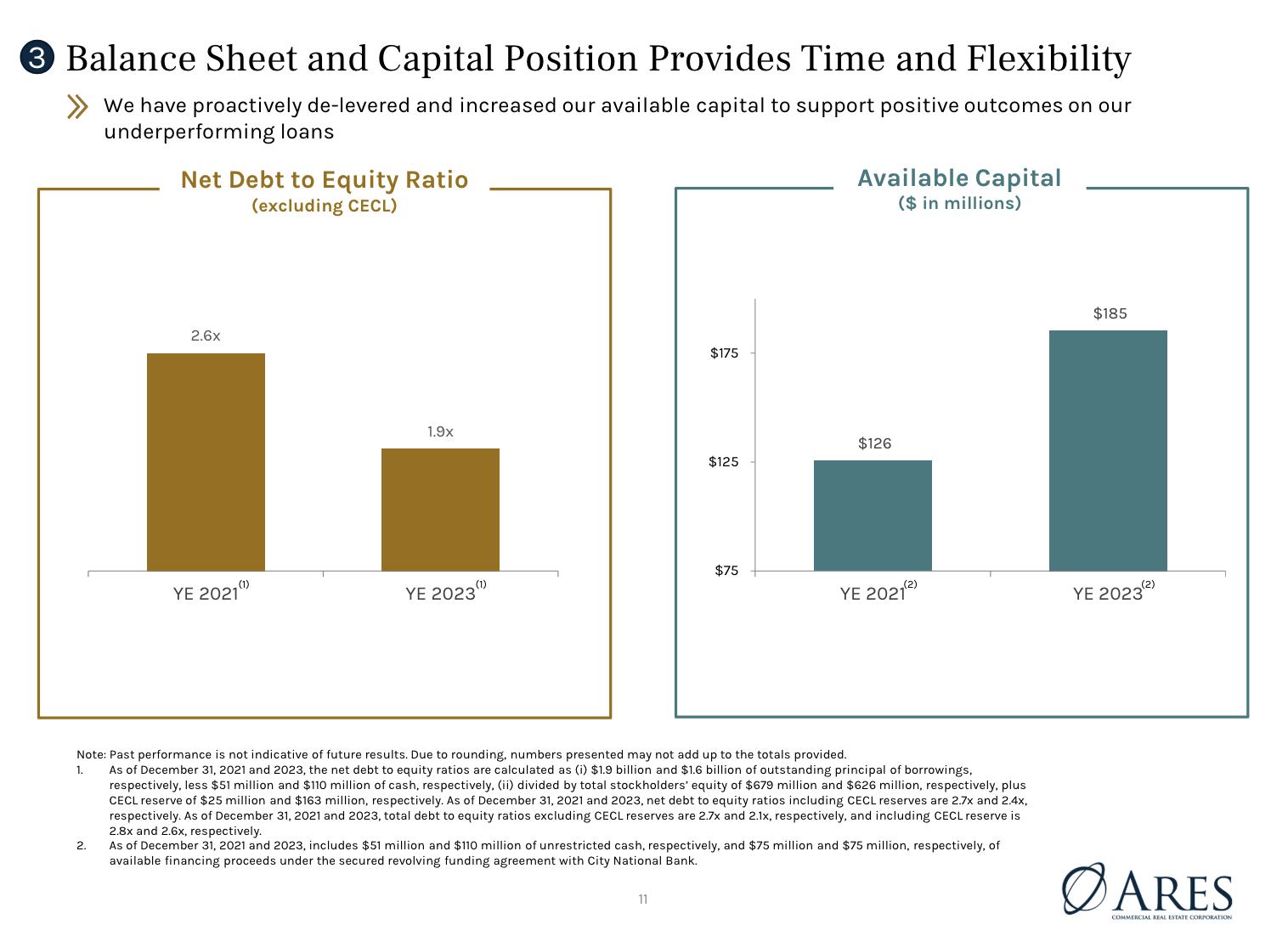

The good news is that the company is increasingly focused on strengthening its liquidity and capital position.

Going into this year, the company maintained significant liquidity, with a moderate net debt-to-equity ratio of 1.9x. Notably, this calculation included the addition of CECL reserves to shareholder equity.

Ares Commercial Real Estate Corporation

{kind=link}

Including CELC reserves, the net debt ratio rises to 2.4x, compared to 2.7x at the end of 2021.

ACRE also has $185 million in undrawn liquidity under its working capital facility.

The good news continues, as the company noted during its earnings call that it sees improvements on the horizon:

Fortunately, we are starting to see some positive trends in the macroeconomic environment that we believe are likely to benefit commercial real estate, including the potential for declining short-term interest rates. Specifically, declining spreads on CMBS and CRE CLOs, particularly during the past 6 months, reflect strengthened capital markets conditions. – ACRE 4Q23 Earnings Call

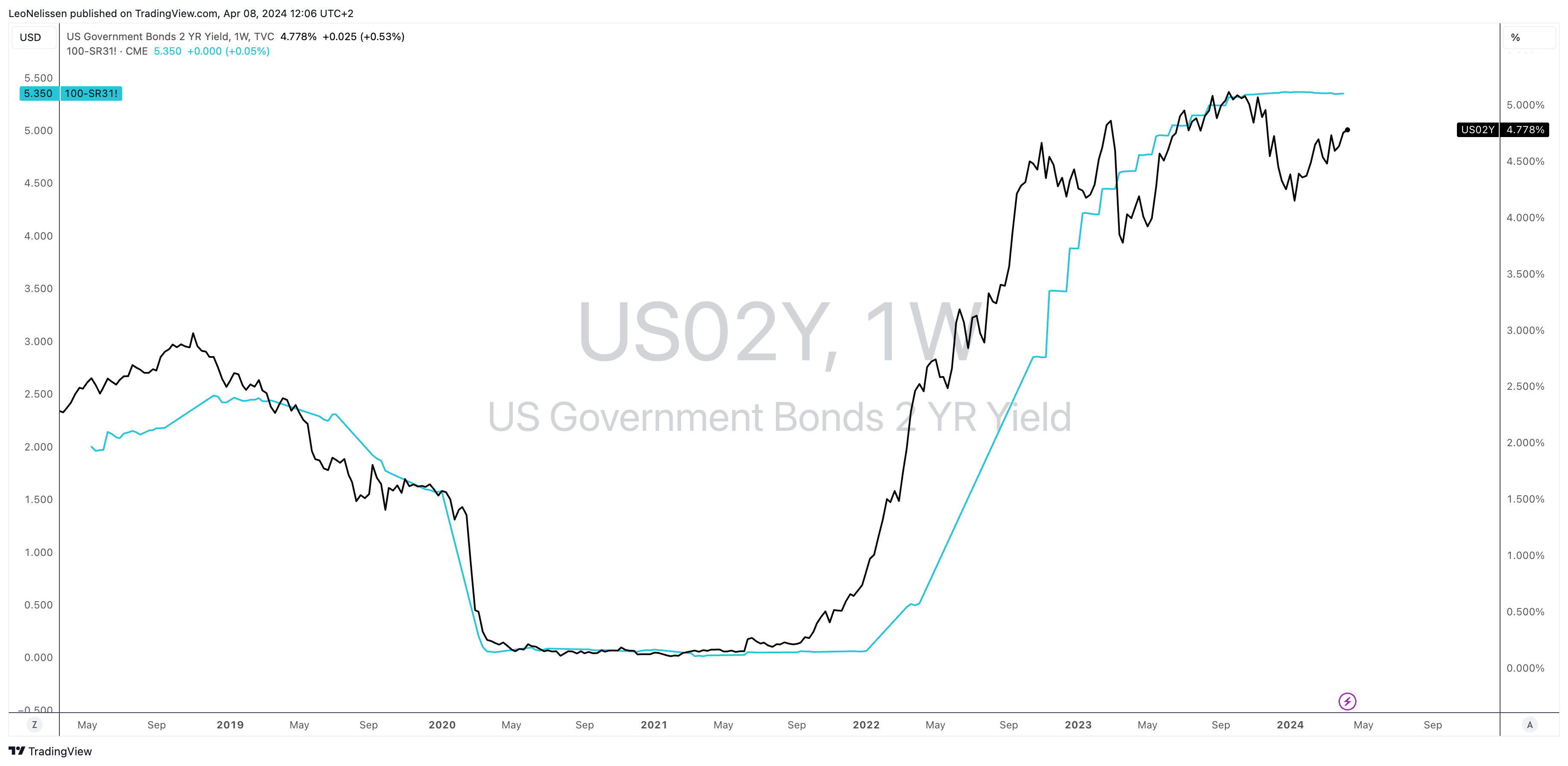

Unfortunately, when the company held its earnings call in February, the market expected the Fed to be much more dovish this year. Since then, rates have bounced back again. The 3-month SOFR rate is still 5.3%, and the 2-year U.S. government bond yields 4.8% again.

TradingView (3M SOFR Rate, U.S. 2-Year Yield)

{kind=link}

Essentially, this is the “higher for longer” environment that makes me a bit nervous.

So, what about the dividend?

The ACRE Dividend & Shareholder Value

As I already mentioned in the intro, the company cut its dividend by 24%. The only reason why ACRE still yields 14% is its poor stock price performance.

The reason behind this is very simple. In light of economic challenges and the need to boost credit reserves, there’s a bigger emphasis on safety than shareholder distributions.

In this current market environment, however, we believe it is in the best interest of ACRE and its stakeholders to reduce the quarterly dividend to help preserve book value and liquidity and to pay out an amount more in line with our expected near-term quarterly distributable earnings before realized losses. Ultimately, as we get through this cycle, [indiscernible] we execute on our earnings opportunities as discussed, we expect we can return to higher levels of profitability. – ACRE 4Q23 Earnings Call

With that said, there’s another problem. In 2023, the company generated $1.06 in distributable earnings (per share). That’s $0.06 above the new annualized dividend of $1.00.

In other words, the payout ratio is still elevated. New headwinds could easily trigger another cut.

Based on its fourth quarter, the company has an earnings power of $0.20, which implies an annual distributable earnings result of $0.80. That’s below its current dividend.

However, based on current measures, the company believes it has the ability to protect the dividend.

And really, as we mentioned, kind of setting our dividend at the $0.25 level for the first quarter of 2024, we did take into account what we believe we can achieve in terms of distributable earnings once we’re able to successfully resolve some of these loans. – ACRE 4Q23 Earnings Call

Valuation-wise, we see that investors have priced in a lot of weakness, as ACRE trades at 62% of its book value. Before these debt issues, the stock traded close to 90% of its book value, which makes sense, given its slightly riskier loan portfolio.

The current consensus price target is $7.70, which is 8% above the current price.

All things considered, I have to say that I decided to give the stock a Sell rating.

This is based on the fact that I’m giving stronger peers like STWD Hold ratings.

As I believe that credit quality will get worse in the quarters ahead, I do not rule out another dividend cut for ACRE and lower stock prices.

Moreover, because of its focus on offices and multifamily assets, I also cannot make the case that it’s a great buy on weakness. If I were looking for exposure in this market, I would pick safer peers, even if these may come with lower turnaround potential if we enter a new bull market for CRE lenders.

So, although I have tremendous respect for ACRE and its parent company, I believe it’s a horrible asset to own in this market.

While I hope I’m wrong, I do not see a scenario where debt quality improves in the quarters ahead, which means we are likely to find out why some high-yielding stocks come with elevated risks.

Let’s hope I’m wrong.

Takeaway

In today’s volatile market, it’s crucial to assess macroeconomic factors like credit quality.

Despite a resilient past, Ares Commercial Real Estate faces challenges due to its heavy exposure to struggling sectors like offices and multifamily properties.

The recent dividend cut and looming credit risks signal more potential turbulence ahead.

While ACRE maintains liquidity and strives for profitability, uncertainties persist in the face of elevated economic headwinds.

As a result, I give the stock a Sell rating.